If your health insurance plan’s benefits involve some type of deductible, this article will help you understand the general terminology involved in your claims, how your charges are generated, the life cycle of a claim, and what to expect with this type of insurance plan. I have to answer a few other questions to get a fully detailed answer to “What is a deductible?” so I hope you don’t mind learning a few other things, as well! There will be too many words below already, so let’s get started!

TERMINOLOGY

I won’t waste space on the literal terms here because our in-network insurers do a good enough job with their dictionary definitions, here:

These definitions don’t add much context to a real-life claims situation, so I’ve included a familiar scenarios to practically interpret or understand the terminology:

Your PREMIUM is a set payment every month to your health insurance company for the right to have health insurance benefits. This is a fixed monthly expense that you owe for at least an entire year, regardless of how often you use healthcare services.

Your COPAY is a static number that applies to certain types of consultations, usually PCP, Specialist, Urgent Cares, and sometimes also Emergency visits. Regardless of the length of visit or topics discussed, you always will owe this amount every time you have a visit.

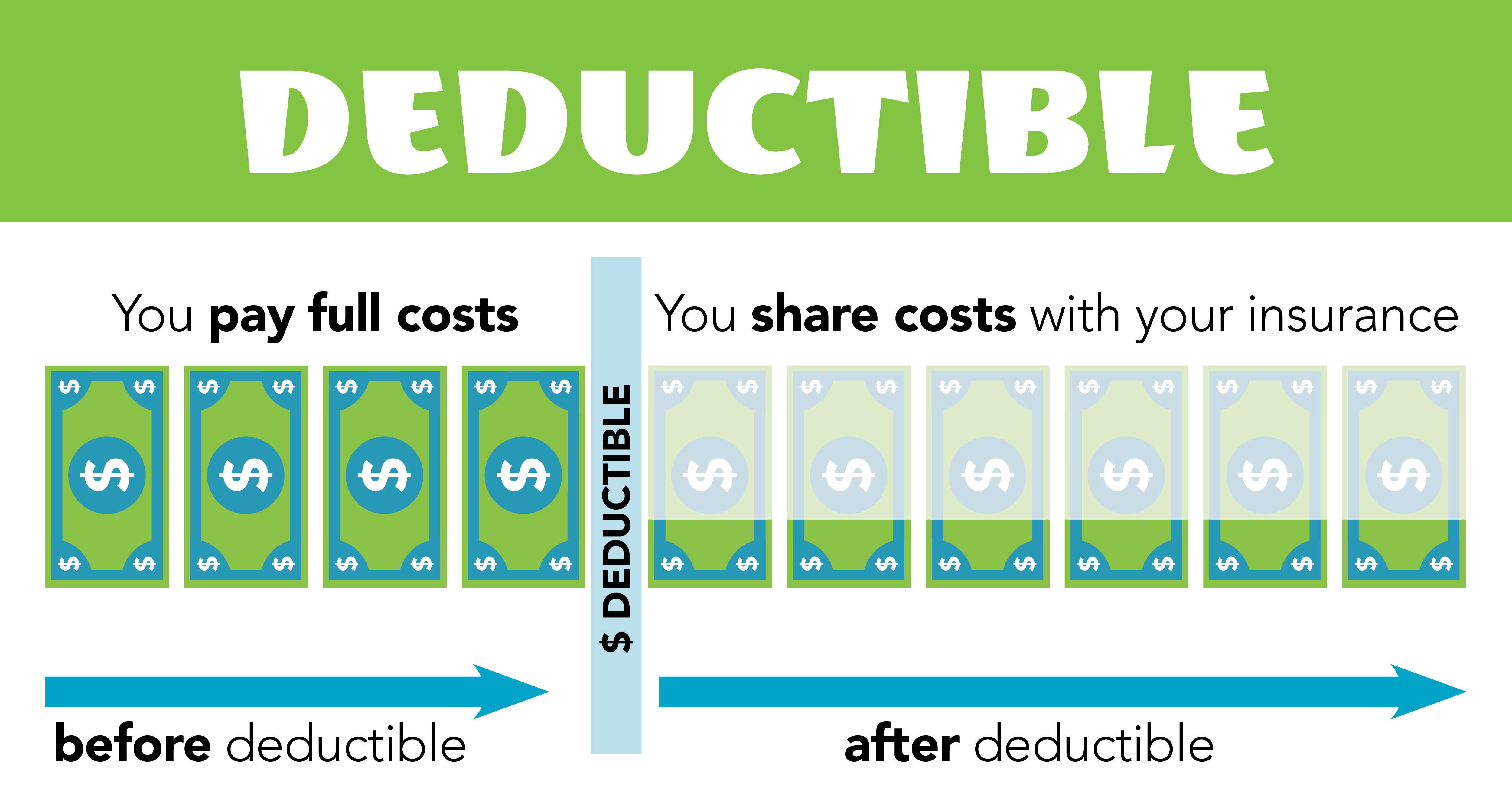

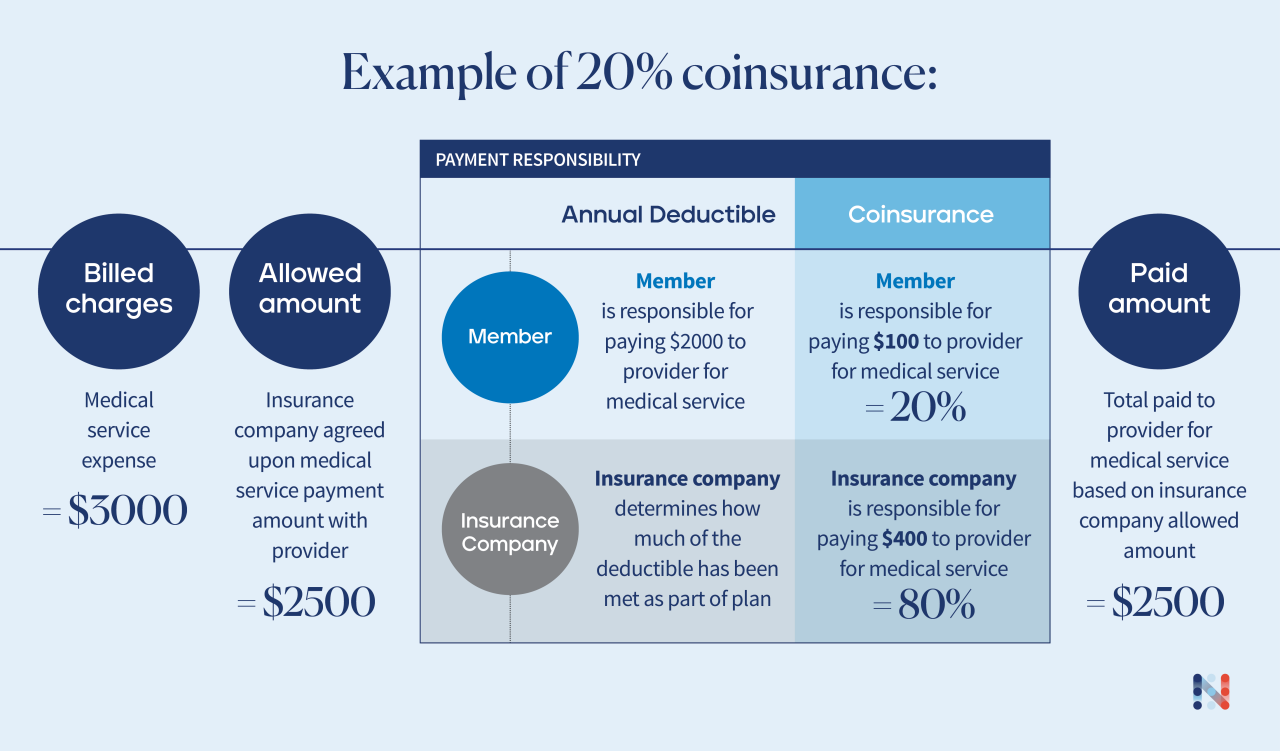

Your DEDUCTIBLE is a variable number that sets an amount of medical expenses that the patient must pay for diagnostic services prior to the insurance company beginning to cover a portion of the same services. Most plans, even plans with Copays, have at least a small deductible for lab services and prescriptions, while others have deductibles that apply to all services.

Your COINSURANCE is a variable percentage that applies to services incurred after your deductible has been met. If you owe 100% of services before your deductible, your coinsurance percentage is the amount you’ll owe after your deductible has been met. You’ll owe this percentage until you meet your Out-of-Pocket Maximum.

Your OUT-OF-POCKET MAXIMUM is the total amount of expenses you can possibly incur for approved medical services over an entire benefit period. Unless you have charges that are non-covered, out-of-network, or otherwise excluded from your benefits (eg. employers not allowing employees coverage for weight loss products), this is the most you’ll pay.

Now that the terms I’ll use below are out of the way, let’s learn more interesting things!

Essentially, the total charge is comprised from 5 factors:

Insurance Company and In-Network Status. Are you in-network or out-of-network? You’ll pay more for out-of-network.

Benefits on Insurance Plan. Do you have a copay-based plan, deductible-based plan, or cost-sharing plan? That will matter.

Length and Content of Visit. Was it a quick, easy visit, or a long, complicated surgery? Longer, more involved visits are generally more expensive.

Preventive or Diagnostic Coding. Was the visit preventive, or diagnostic? Preventive visits are usually free, diagnostic visits are more expensive.

Services Provided. Did you also have labs, procedures, vaccines, etc. with your visit? Those will add costs.

For a frame of reference, here is a listing of our uninsured prices for most services at Family Care. Each insurance has their own fee schedule and rate of reimbursement, but these are good ranges to expect for commercial insurances.

THE LIFE CYCLE OF A HEALTH INSURANCE CLAIM

It is important to understand the timing and steps involved in a health insurance claim process so you do not waste more time than necessary dealing with your insurer. It’s already terrible enough to call, knowing you’ll spend longer than necessary listening to the most annoying hold music science can create, and it’s even worse if you call for no reason. Basically, insurance claims require patience because they intentionally delay things on purpose to drive you crazy, so knowing where you are at in the timeline can save you a lot of stress!

These are the basic steps involved in a claim. A workflow diagram would probably be appropriate here, but this will have to do for now:

The Visit (Day 0). This is the interaction where you received a billable medical service. This is thing you did that requires payment to a medical provider. You were probably sick that day, so I hope you’re feeling better now!

The Claim (Day 7-10). Family Care waits 7-10 days to submit a claim to a health insurance, but this delay is not universal. The main reason that our office waits is to allow patients time to ask and address any follow up questions to their visit under a single billable encounter. This policy is designed to reduce overall patient expense and eliminates one of the barriers to positive outcomes by encouraging the patient to ask questions they forgot or notify our staff immediately if a treatment is not going well.

The Patient Response (Day 24-40). This period is when you will first receive a statement from your insurer after having a medical visit at our office. An Explanation of Benefits (EOB) will have the first determination of coverage and explains how your benefits applied to the medical service you received. There will be a Remark Code that represents the coverage determination reasoning – if you owe any money for a medical service, this remark will explain why. It will probably be short and incomplete, which is designed to either make you misunderstand the reason or give your insurer a lot of wiggle room to explain how they applied their reasoning. If you disagree with any coverage determination, this is your head-start on fixing the issue before you receive an invoice.

The Provider Response (Day 31-47). About a week after you receive your EOB from your insurance, your provider receives their own statement, called an Explanation of Payment (EOP). This is when our office would find out that you owe us money. This is essentially identical to your EOB statement, but with many other patients on the same file and fewer specific details on each patient’s individual benefits.

The Invoice (Day 38-54). Within a week of our office receiving the EOP for your claim, you will receive an electronic invoice for any balances due. This will be sent to the email address we have on file for you. You will receive reminders every two weeks and start to incur late fees after 90 days, unless you are actively appealing a denial.

The Appeal (Day 45-90). Insurers will consider coverage appeals within the first 90 days after processing a claim. If you disagree with the benefits applied to your claim, you will need to file a formal appeal. The appeal process is different for all insurers, but it should be detailed on your EOB from Step #3. If you appeal, please notify our office and we can help guide you to avoid wasting more time making unnecessary appeal attempts.

As a general rule, insurers take about 30 days for absolutely every decision. If you file an appeal, there is almost no point in following up within 30 days of the submission. You will likely just be told that it is in process and to call back again, so skip that step and just be patient!

WHAT WILL ACTUALLY HAPPEN WHEN I VISIT MY PROVIDER

Terms and theories are great, but knowing what will actually happen to you is better! These are basic examples of three common situations – you owe a deductible balance that you agree with, you owe a deductible balance that you disagree with, or your claim is denied completely.

In all of these scenarios, you would have already received some type of medical care and have an insurance plan that features a deductible-based benefits plan.

Deductible Owed (Correct).

If you receive your EOB and agree with the balance due, you just need to pay your bill! If you already paid at the time of service, you’re probably done with the transaction. If you have not yet paid, you should expect a bill in about a week. This should be what happens >95% of the time.

Deductible Owed (Incorrect).

If you receive your EOB and disagree with the balance due, there are two probable reasons why you disagree:

The EOB says you owe less than you were billed, or less than you already paid. There are a lot of reasons this could have happened, but as long as everything that was denied was a “covered service” it likely means you’ll end up with a credit or refund back from your provider. In most cases, you likely met your deductible either before or during the claim in question, when it is generally impossible to tell which claims insurers will process first. You’ll end up owing the same deductible amount, but the provider that you have to pay that amount to might change based on the timing of the claims.

The EOB says you owe more than you were billed, or more than you expected to owe. Similarly, there are also plenty of reasons this could have happened. There will be a remark code underneath the claim table that explains why something was denied or not paid. Depending on this reasoning, you can either review your coverage with your insurer or review the claim’s coding with your provider.

Claim is Denied.

This is a light grey area where the total you might owe the provider is the same, but you are not getting credit towards your deductible.

eg. A denied service costs $100. Your provider bills you $100. If it was covered, your $5,000 deductible would then go down to $4,900, saving you $100 by the end of the year. If it was denied, the charges don’t get applied to your deductible and you still owe $100, so it’s basically like having a $5,100 deductible at that point. Obviously, that is worse.

In general, you’ll want all charges to be “approved,” even if you end up having to pay for them. The denial remark codes will explain your next possible steps towards getting a denied service reversed and approved.

When in doubt, contact your provider. We usually receive our version of your claim statements about a week after you do, so don’t freak out immediately when receiving a scary EOB. We can definitely get started on fixing issues before we receive our own statements, but just remember that we might not yet be aware something went wrong with your claim and will need a bit of time to help identify the issue. There is a general strategy to fixing every type of problem, but understanding what those problems look like and identifying how they happen should hopefully provide the tools necessary to defeat your insurance denial and receive the most from your insurance benefits.

What happens when you visit a Non-Participating Provider with Medicare?

Family Care is a non-participating provider with Medicare, which basically means we do not accept assignment (ie. receive money) from any Medicare program. This is a brief summary of what that means from Medicare.gov:

You might have to pay the entire charge at the time of service. Your doctor, provider, or supplier is supposed to submit a claim to Medicare for any Medicare-covered services they provide to you.

They can’t charge you for submitting a claim. If they do not submit the Medicare claim once you ask them to, call 1‑800‑MEDICARE.

They can charge you more than the Medicare-approved amount, but there is a limit called “the limiting charge “. The provider can only charge you up to 15% over the amount that non-participating providers are paid. Non-participating providers are paid 95% of the fee schedule amount.

While most non-participating providers will force you to leave the practice, we allow new Medicare patients to remain at our practice because we do not think insurance companies, even Medicare, should dictate who you are allowed to see as your primary care provider. Family Care will attempt to make the process simple, but there are some unavoidable downsides you should expect when considering remaining as patient and visit a non-participating Medicare provider:

You will be required to pay up front for your visits. You pay us, we file your claim, Medicare pays you. These claims are included in your Quarterly Beneficiary Notice and any payments for approved services will be made directly to you, not to our office.

You will need to wait 1-3 months for reimbursement. The full claims process usually takes 4-6 weeks, but Medicare should reimburse you ~70-90% of the amount you paid.

If you pay us $100, we expect you to receive a ~$80 check from Medicare.

Most services will cost ~10%-15% more than normal. An average Medicare visit costs $100, so you can expect to pay $7-$12 more per visit every time you have an appointment.

If a service costs $100, you would probably only owe ~$10 at a participating provider, but you would end up owing ~$20 at Family Care.

We want what is best for our patients, even if that means helping them transition care to another primary care provider. We understand that this arrangement may not work for all patients and they might prefer a simpler process with an in-network / participating provider, instead. We are extremely grateful that many of our patients like our providers so much that they are willing to deal with these changes and remain patients at our practice. If you do wish to change providers, we can easily transfer your records to help make a smooth transition to a new provider.

To give you some positive news, here are a few reasons why you might want to stay as a patient, even though we do not accept your new Medicare insurance:

We still file your claims with Medicare. You should not have to do any paperwork to submit your claims; you will only need to notify us in the event of a denial or non-payment so we can fix the issue.

We will help you read your Beneficiary Notices. Every three months, Medicare will send you a summary of all charges incurred during the previous period. If you have any questions, Ryan would be glad to review the document with you to help you understand what happened.

Our lab accepts Medicare. You will not have any additional costs or problems associated with a non-participating provider status for all lab samples and testing. These services would be processed as in-network with your Medicare plan and would be the same anywhere you go.

Your Welcome to Medicare Exam is still covered. This initial screening within the first six months of your enrollment date has the same level of benefits for participating or non-participating providers.

You can keep your provider. If you’ve been with us for a long time, we will be sad to see you leave!

We understand that learning the Medicare process can be like learning a new language. Their statements, forms, and processes are quite different than most commercial insurances, so there will be a learning process in the beginning regardless of where you go for care. You will experience many changes just because you are on Medicare, and then we add more exceptions to the rules because we are non-participating, so it can be a confusing process at first. If you remain as a patient, our hope is that we can make the process easy and clear. We will help guide you through the process so you are an expert on your Medicare coverage after you first couple of visits.

If you have any questions at any point during your transition, please ask Ryan!

3 Things to Consider When Signing Up For Health Insurance

The problem that most people have with their health insurance plan is rarely with the actual coverage – people are generally only upset when their plan doesn’t cover something they thought it would or when they are surprised by some costly detail that wasn’t made clear at enrollment. Insurance companies don’t do the best job of educating patients on the actual details of the plans they are selling, but the information you need to know to set proper expectations is available if you know where to look. You’ll have to do some work and learn some pretty boring things, but you are the one who ultimately has to understand the details of your plan’s coverage, not your insurer. The point of this article is to help you understand the crucial differences between possible plans and help you feel comfortable with the coverage you choose.

The entire concept of health insurance is that you are basically making a bet on your health. The healthier you are, the less likely you are to use your insurance for high cost medical services. Your insurance company knows this and sets their prices accordingly. If the insurance company thinks you are going to cost $5,000 to cover this year, their goal is to set your total premiums and out-of-pocket expenses to more than $5,000 so they can make a profit.

This is the bet –who will get the better deal once all of your medical expenses have been paid?

The benefit structure of every plan offered by insurers is carefully calculated to give them the best chance of winning this bet. By understanding how your insurance plan works, you can put the odds back in your favor and make every dollar you have to spend on healthcare go much further.

There are three broad categories to consider when signing up for a new health insurance plan:

Cost – How much will I pay in out-of-pocket expenses?

Coverage – What services and medications will I have access to under my plan?

Network – Is my provider “in-network” with my insurance plan?

Each component is equally important and can have critical implications on the others. While it is almost impossible to get your expected costs 100% right before things actually happen, just having a very good estimate will help you budget accordingly and avoid surprises when you seek medical care. If you need help with this calculation, our Health Insurance Cost Estimator Tool should help give you a good estimate.

I hope the following pages will help you fully understand the benefits, and consequences, of your choices when you’re deciding between two possible plans.

Continue reading to go into further detail on each one of these components.

COST – How much will I pay in out-of-pocket expenses?

The most popular way to think about the cost of your health insurance plan is to focus on the monthly premium. This sounds good because you know the fixed costs associated with your plan and can seemingly predict exactly how much you will have to spend for coverage. However, this line of thinking leaves out the most important part by ignoring the variable costs a person might incur each year when they actually use their health insurance and visit their doctor.

To get a complete picture, you should compare a plan’s total expected out-of-pocket expenses, which factor in the possible copayments, coinsurances, and deductibles that you might have to pay for during the year in addition to your premiums. Signing up for insurance and paying your premiums to your insurer is not the only out-of-pocket expense you should expect if you need medical care. Much like car loan payments don’t cover the cost of the gas you need to put in the car, different health insurance plans might require significantly more “gas” than others if you actually want to take your plan out for a drive.

There are two primary things to consider when comparing the cost of two different plans – how much you’ll actually use your insurance, and how much you’ll have to pay in a “worst case scenario.” It is also important to remember that the out-of-pocket maximum does not include premium payments. Here is a quick plan comparison as an example.

Plan A:Higher Premium, Lower Out-of-PocketIf you have some chronic conditions that require frequent visits to specialists and take some high priced medicines, it will probably end up being cheaper to pay a higher premium for better coverage. Since you’ll be using the insurance often, it is comforting to know you’ll have a low limit on out-of-pocket costs when you actually need care. However, if you don’t end up using your insurance as much as you thought, you’ll be paying significantly more for unnecessary coverage.

Plan B:Lower Premium, Higher Out-of-PocketIf you are relatively healthy and rarely visit the doctor, a cheap premium with a high deductible makes sense because you want the lowest fixed costs possible. By not seeking medical care often, you can be pretty sure your variable costs will be low. You leave yourself more vulnerable to higher costs if something bad were to happen, like an unexpected emergency room visit or hospital admission, but that is a part of the bet you’re placing on your care.

Now to the fun part – Charts! Woo!

This chart compares the total cost of the healthcare you need with the total out-of-pocket expenses incurred if you were covered under either Plan A and Plan B. Because Plan A has a higher premium, the fixed cost of this plan has a higher floor than Plan B. If you don’t actually need to use the insurance, you will save money by choosing Plan B. The turning point occurs when the two lines intersect, which in this comparison is just over $4,000 in total health expenses. At that point, you’ll be saving money by choosing Plan A, even though the premiums will be more expensive.

Remember that “bet” we talked about earlier between you and your insurance company for who has to pay more of your healthcare expenses? The grey line represents the actual expense incurred to keep you healthy. As you can tell, the insurer is hoping they have enough members incur less than about $7,500 in health expenses each year to pay for the few members who will be extremely expensive to cover. The insurance wants to move that break-even point as far to the right of the chart as possible, while you’re hoping to intersect with their line as close to the left as possible.

Because it is impossible to predict the future and know exactly what services you’ll need, the best way to look at something like this is in terms of a “Best Case” / “Worst Case” scenario.

In a “Best Case” Scenario, where this person is perfectly healthy and never uses their insurance plan at all, Plan A will be twice as expensive as Plan B ($4,800 vs. $2,400) because the premiums are guaranteed payments regardless of how often you use your insurance plan. Plan A will actually still be more expensive than Plan B, overall, all the way up to the first $4,000 in out-of-pocket expenses. If you are unlikely to have at least $4,000 or more in annual health expenses, it makes sense to pay a lower premium and pay more of your own out-of-pocket expenses. Plan B would be a better choice as long as your expenses were lower than $4,000 during the year.

In a “Worst Case” Scenario, where this person ends up in the hospital for at least a few days and racks up $50,000+ in medical expenses, Plan B will be up to $2,600 more expensive because there is a higher deductible and out-of-pocket maximum limitation. The ACA put a cap on the out-of-pocket maximum that a patient would have to pay in such a situation, so the out-of-pocket maximum helps provide a safety net to ensure people don’t go bankrupt due to a medical emergency. In this case, Plan A would have better coverage.

These are overly simplified examples, but it shows how the total cost of healthcare for an individual can vary greatly just based on the type of plan they choose. Most likely, you will fall somewhere in the middle of the “Best Case” / “Worst Case” spectrum. The goal is to guess how close you are to one side or the other and how likely it is that you’ll need a high cost service during the year. You obviously can’t plan on having a serious accident, but the closer you get to that tipping point between the two plans, the more you might want to consider increasing your coverage to feel a little more comfortable with your financial risk in such a situation.

COVERAGE – What services and medications will I have access to under my plan?

There are several different ways to define “Coverage” when you’re referring to the details of an insurance plan, but this section will focus on the specific procedures, treatments, and prescriptions that your health insurance plan will approve. Basically, if you have a problem and you sign up for an insurance plan, you want to make sure that specific problem is something that falls under the benefits outlined in your plan.

The majority of what is required to be covered by insurances is either mandated by the Affordable Cart Act or derived from basic Medicare standards, so most of coverage details for medical services are the same across the major commercial insurers. But, that doesn’t mean they are all the same, either. Standard medical services like doctor’s visits, generic medications, and vaccines, will be accepted on almost any plan. However, if you are planning to do non-standard things, like cosmetic surgeries, treatment for rare or complex diagnoses, or special blood testing, you should really try to dig a little deeper into the plan to see what types of services are actually covered.

Essentially, the best way to think about how to get the “best” coverage you need is to start by seeking coverage for your most expensive service. Call your providers and ask for a price quote for certain types of visits you expect to incur during the benefit year. You will probably never get a definite answer (for a variety of really good reasons that we’ll answer in another post), but you should be able to get a ballpark idea what kind of prices you can expect. Ask for the specific CPT Codes that will be used for your procedures so you can tell your insurer exactly what you want to verify. Then, figure out which insurance plan covers the services that would cost the most if you didn’t have coverage because they will make the biggest difference in your bottom line for out-of-pocket expenses.

Here is a simplified chart that helps you visualize the types of priorities you should be making when selecting coverage. These are just working estimates and are by no means exact, especially considering that we just spent 1,000 words earlier in this article talking about how the “Cost If Covered” part of the equation could vary drastically depending on your plan. The point is to get a sense of the risk involved in having, or not having, coverage for a particular service.

Obviously, having coverage for the ER visits would be Priority #1 in this scenario. A single accident with no coverage could be financially devastating. But, those are generally few and far between for most people. Again, this goes back to the concept of placing a bet on your health expenses. You should go down the list of your expected health costs and find a plan that will pay for all of your highest priced items first, since they will have the biggest net difference on your potential bottom line.

After all, what would be worse? Having to pay an extra $75 because a PCP visit was denied, or having to pay an extra $45,000 because your hospital visit was denied? A PCP visit is more likely to occur, but the one time the hospital visit gets denied will potentially be the most devastating. However, because denials are still not too common if you have insurance, the most common factor that comes up when differentiating plans based on their overall coverage relates to prescriptions, as they can vary greatly depending on the plan.

Prescription Coverage Details

One plan could offer a certain drug at a $10 copay, while another plan might not cover it at all and either cost you $200 out-of-pocket or force you to switch to a different medication that your insurance prefers. Neither option is ideal, as you’re ultimately either poorer or sicker if your medication isn’t covered by your insurance. The insurers structure their drug coverage decisions based on the population of their insured, so finding the plan that best suits your patient profile could make a big difference in prescription costs.

So, how do you find out which drugs are covered on which plan?

To be confident in your choice, you should learn the details of the prospective plan’s drug formulary. Most of the time, a simple Google search with “Name of Insurance Plan, Drug Formulary List” in the search box will direct you to a PDF of the plan’s details. If not, there should a link on the insurance provider’s website or a phone number you can call to request a copy by mail or email. Prescriptions are one of the few health expenses you can make an accurate budget for up front, so it is important to know how your plan will cover the medications you are currently taking.

If you think your medication may be too expensive, even with commercial insurance, there may be programs that you can sign up for to reduce the cost. Please contact our office to discuss potential coupons, savings programs, and rebates that may be available for your medication. There are a lot of programs available to receive discounted prices on your medications, so it is ultimately in your best interest to take advantage of them when you can. If you are a current patient, ask for details!

NETWORK – Is my provider “in-network” with my insurance plan?

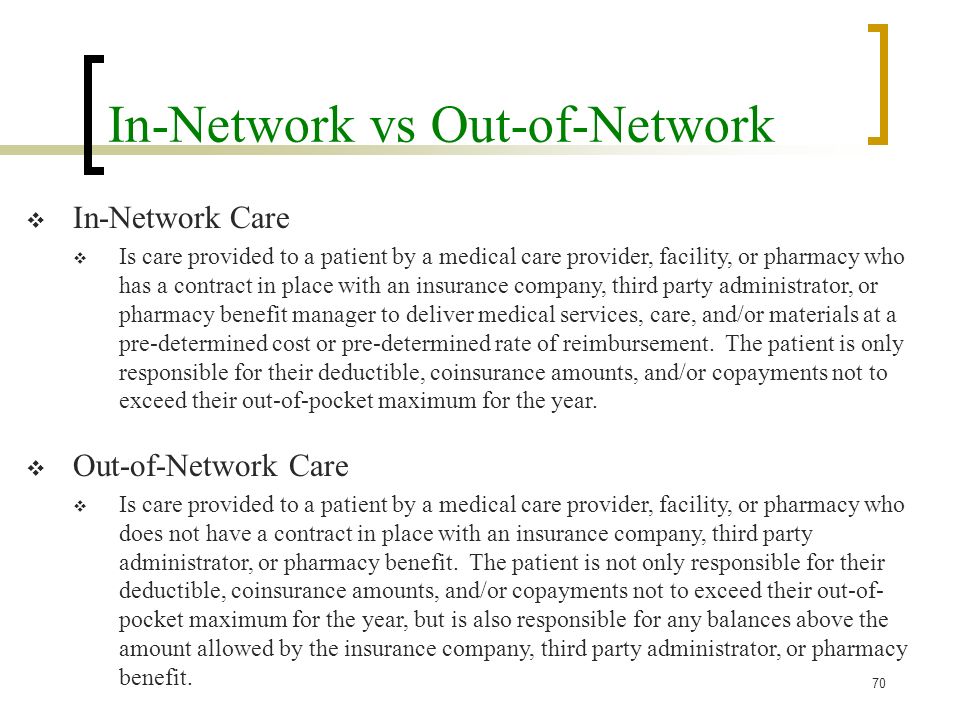

If you already have certain medical providers you prefer and want to make sure you’ll still have access to those providers, you’ll want to sign up for a plan that is accepted as an in-network insurance by your provider. If you stay in their provider network, the benefits on your plan will actually apply to your visits and you’ll receive a much lower rate than you would if you went out-of-network.

Because a person may see multiple providers and every provider has their own list of accepted insurances, you may run into a problem finding a single plan that is accepted by all of your preferred providers. Or, once you find that plan, you realize it is just way too expensive and cannot afford to sign up, so it is effectively inaccessible. In this situation, you’re going to need to make some type of compromise. You should start by assessing the true cost of the care you expect to receive and focusing on your largest possible expenses first.

No matter where the line of “affordability” lies, it is obvious that a PCP visit is at least “more affordable” than an emergency room visit. If you had to pay for one of those yourself, you’d much rather it be the $100 PCP visit rather than the $5,000 ER visit. While you can still manage to incur some pretty significant medical costs with frequent primary care offices and specialists, the out-of-pocket expenses will never be on the same level as a single visit to the hospital. Because primary care visits at Family Care average around $100 per visit if they are not covered, you’d have to have non-covered primary care visits twice a week for an entire year to match the cost of a single accident that landed you in the hospital.

With most health expenses, the bills escalate quickly due to a few common types of services:

Hospital Visits. Just one night in the hospital could cost more than $10,000 if you don’t have insurance, so these visits create the majority of medical debt.

Surgeries. A single surgery can sometimes cost more than $5,000 and often requires several costly follow up visits to make sure you are recovering well.

Tiered Medications. For drugs that have very specific indications or are considered upper-tier level medications, out-of-pocket costs can be up to $1,000 per month.

Because we are dealing with a situation where the insurance company is putting the obligation to pay the claim on the patient, this is basically an extension of our previous discussion on covered services, in general. Being “out-of-network” is one of the most commonly used reasons for an insurer to deny coverage for a particular service, so your plan’s network really has a big influence on your expected out-of-pocket expenses for a certain service. For example, the price of the same EKG at an out-of-network cardiologist could be 500% more expensive than if it were performed by an in-network cardiologist. That is actually kind of crazy when you think about it, but that is for another article.

There are a few different ways to find out which providers are in your network.

Call your insurance company. There is always a customer service number you can call to speak with a representative from your insurance. Ask them to send you a list of the providers in your area that accept your insurance. Usually, they will either read you a list over the phone, email you PDF file, or direct you to the content on their website.

Visit your insurer’s website. Most insurance plans have a “Provider Finder” tool somewhere on their website. Make sure you select the proper choices from all of the possible search filters to ensure that the list actually applies to your plan.

Call the provider. Each provider will know which plans they accept, so you could ask them as a starting point. Make sure know the name of the company (eg. BCBS, Cigna) and the name of the specific plan (eg. Blue Advantage, Choice Plus), as both of those are required to verify your coverage. Even if the provider says they accept your plan, you may want to double check with the insurer, anyway, as they will be the ones to ultimately process your claim and make that decision.

In order to maximize the amount of coverage you receive from your plan, you should try to stay “in-network” for as many services as possible. Plan to be “in-network” for the big expenses first, because that will make the most difference in your yearly out-of-pocket spending. There are many plans that actually offer pretty good out-of-network benefits, but they will still always be at least some margin less than your in-network benefits.

TLDR – A summary of the most important pieces of this article.

To summarize the last 3000 words, here are the main points I hope you learned from this article:

Your monthly premium is not the only factor you should consider when signing up for an insurance plan. You should consider your total out-of-pocket expenses, which include any copayments, coinsurances, and deductibles associated with the plan you choose.

The amount of money you have to pay each year can vary dramatically from one plan to another. You should try to estimate your expected health expenses for the year and find a plan that works for you.

You should seek coverage for your highest priced services first, and then worry about the lower priced items later. It is much easier to pay a $100 PCP visit out-of-pocket than it is to pay a $5,000 hospital bill.

If you are on medication for a chronic condition, you should ask to see a prescription drug formulary for your prospective plan to ensure that the medication you need will be covered by the plan you choose.

You should try to visit in-network providers whenever possible. Going out-of-network can significantly reduce the amount of benefits you will receive from your insurance plan.

If you are a current patient at Family Care and have any questions, you should ask Ryan for help! Contact us here.

VIDEOS – You prefer to watch videos about health insurance instead of reading articles? OK!

Because I completely understand that most people consider insurance to be completely boring and tedious, I tried to select some fun insurance education videos that I thought were actually pretty entertaining. These videos cover similar concepts to what we just discussed in this post and help emphasize the most important point of this whole article – that health insurance can be a good thing that actually make sense and occasionally helps you out, if you know what you’re doing. I hope you learn something that helps you even the playing field and get the most out of your coverage.

HUMANA – “How Do Deductibles and Copays Work?”

This is a really cool whiteboard “explainer” video on the different possible ways you could incur out-of-pocket expenses. I think this video does a good job on the concept of out-of-pocket maximums and deductibles, while making you really care for Gina as a person. At 1:59 in the video, I blame whoever was supposed to be spotting Gina on the ladder for that accident. It is also pretty cruel to just leave Gina on the ground while telling her she owes 20% of her medical bill for the fall. C’mon, video guy.

KAISER FAMILY FOUNDATION – “Health Insurance Explained – The YouToons Have It Covered”

This video covers the interesting journey of a beanie-wearing skateboarder that signs up for health insurance and gets into an accident because of a thieving raccoon. The video does a really good job explaining the risk factors involved with not having insurance and understanding the value of staying in-network for services. In the end, you’re actually a little bit upset the hero of the story didn’t learn from his experience when he chases after the raccoon again. You’re gonna get hurt again, dude! Let the raccoon go!

“MILIMAN, INC – Understanding healthcare costs: The employer-sponsored insurance system”

For the roughly 2/3 of people who don’t really care about the individual healthcare marketplace because they have health insurance through their employer, this video is for you. This helps explain the reason your premiums rise, or why your employer changes your plan every year to put more of the cost burden on the employee’s out-of-pocket expenses. Most of the time, if your individual contribution is increasing, your employer’s contribution is also increasing. It might not always be at the same rate, but just something to think about so you don’t always have to blame your company for being evil. The video also has a little bit of a “Tron” feel to it, so that is also kind of cool.

“GOATS ON A STEEL RIBBON” – Goats On a Steel Ribbon.”

You’ve probably had enough about insurance for one day, so you deserve a treat. These are goats on a steel ribbon. It is hilarious and mesmerizing and I really wanted the big goat to jump on the ribbon. I like to imagine that big goat jumped up on the ribbon just after the camera stopped recording and he is still there today, happier than all the goats in the land. You can do it, big goat!

Family Care, PA is a primary care medical facility located in the Durham, North Carolina. We understand that there are a lot of options for primary care in the area, so we know we need to provide a great service if we want to earn your trust. The large local hospitals are still very good, but we think that we provide a special type of care and attention to every patient that is not possible inside such a large system. Here are a few of the reasons we think you would really enjoy having Family Care as your primary care provider.

We get to know you personally. Our medical staff and providers take the time to get to know you during your visit, rather than rushing you through your appointment. You will never feel rushed during your visit and will have the opportunity to fully explain your symptoms and concerns. Our administrative staff also takes the time to get to know our patients and works with them to overcome common healthcare hurdles like coordinating specialist referrals, obtaining prior authorizations, requesting medical records, and appealing claim denials.

We are great patient advocates. At Family Care, being the best advocates possible for our patients is always our priority. When coordinating care, we always try to work within the structure of your insurance coverage to make sure the process is smooth and you are able to receive the full extent of your plan’s benefits. Our office policies regarding scheduling appointments, payments, and paperwork are all designed to provide the most efficient and affordable care possible.

We utilize available technology. Our office is able to provide efficient care by taking advantage of the wealth of technology available in healthcare today. We use an Electronic Medical Records system to manage our practice, which features an online patient portal. The portal provides 24-hour per day access to their own medical records at our office, including appointment reminders, prescription directions, and historical lab results.

We schedule 30 minute appointments. Unlike most primary care offices, we schedule each of our visits in 30 minute blocks of time. This does not always mean your visit will actually take a full 30 minutes, but the extra allowance does help make sure you are seen on time for your appointments and still have plenty of room to explain the full nature of your visit and concerns to your provider.

We are up front about our policies. We try to make the processes for how we provide efficient medical care as open and transparent as possible so our patients can understand the reasons behind them and why they are necessary, and beneficial, for our patients. We do our best to help patients understand their insurance policies and are always open about expectations, likely possibilities, and potential problems with obtaining coverage in certain situations.

We are able to be contacted easily. If there is anything else you need to know, just call our office at 919-544-6461. Family Care does not use a “phone tree” or automated operating system, so a real employee at our real office will pick up the phone when you have a question. If we aren’t able to answer the call, it is simply because we are at lunch (12pm – 1pm), or are helping another one of our patients in the office. If you leave a message, we will call you back shortly. Or, you can also contact us by…

Signing up for our patient portal and submitting a message directly to your provider through our EMR system.

Flying a drone to GPS coordinates “Latitude: 35.915967, Longitude: -78.894075″ with your hand-written message. Please print.

Note: Mention this option at your next visit and Ryan will give you a piece of candy.

We are grateful for the opportunity to take part in your medical care. We understand that you have plenty of options available to you – Durham is the “City of Medicine,” after all. We try to help in every way possible and hope you truly enjoy visiting our office. Thank you for giving us a chance to provide you with great medical care!

As of February 10, 2016, Family Care is now considered an in-network provider with United Healthcare! For all United Healthcare patients at our office, this means…

Visits at our office will now be subject to your in-network benefits on your insurance plan. You will now have full access to the benefits on your plan for services at our office!

In-Network co-payments, co-insurances, and deductibles will apply to your visits. No more high out-of-network deductibles!

For an average patient that came in every three months as an out-of-network patient, this means out-of-pocket savings of anywhere from $150 (for high-deductible plans) to $400 (for regular co-payment plans)!

Why did we decide to re-join the UHC network?

If you have recently signed up for health insurance on the individual marketplace, you may have noticed that there are far fewer options available to you than there have been in years past. For the 27713 zip code, and most of the surrounding zip codes, BCBS has limited their available products on the individual marketplace to their Blue Value and Blue Local plans only. Because the Value and Local plans are affiliated with the UNC and Duke healthcare systems (and our office is fully independent), many of our patients were left without an option that would be considered “in-network” at our office.

Now, after signing an in-network contract with UHC, patients who sign up for insurance on the individual marketplace have the option of selecting a United Healthcare plan to receive in-network insurance benefits for visits at our office. We hope this helps our patients save money and get the most out of their healthcare budget.

{kind=link}