The transcript below is a real email conversation I had with a patient who was trying to appeal a denied service. Reading this might help you avoid some of the delays we had with the appeal denial process and give you some direction on the steps you need to take if you want to file a claim appeal. The example refers to CPT Code 93880, which is a CIMT test performed at our office and often denied by out-of-state health insurance companies. You can potentially adapt the conversation to any CPT code, service, and price, as the process is very similar for appealing almost any denied service.

ME: We just received a denial for your CIMT test from February stating it was a “non-covered service” on your plan. That is the only information we received on our end – would you possibly be able to share the information on your statement with me so I can figure out if there is anything we can do for the appeal denial? Depending on why they determined it to be “non-covered,” we may have a few options available to get it covered. Thanks!

PATIENT: How much is it if it isn’t covered? I could dig into it a bit more, but if it’s hundreds of dollars, I’ll be extra motivated. 🙂 Are they usually covered by patients’ coverage?

ME: Yeah, it is usually covered. I was surprised to get the denial. It was $198.65, so it’ll probably be worth trying. I kind of enjoy trying to win these appeals, so I hope you’ll give it a shot! 🙂

PATIENT: I’d love to give it a shot! I’ll put that $200 to much better use. Is there any information I can send along in the meantime? I have had poor cholesterol and my family has a history of heart disease. The test revealed some unfortunate news about my “arterial age” and led to a cardiologist visit. Does that help my case? 🙂

ME: Your EOB from your insurance will probably have more details – I have attached the version I received on my end. Can you see what details yours shows? I’m not sending you an invoice since I think we can get it covered, but I can if that might help. A letter of medical necessity is one of the last options we have for an appeal, so that information should help if we get to that point. Hope it is easier than that, but we’ll see what your EOB says and go from there. Thanks!

Eight Weeks Later (Act 2)

PATIENT: Still no EOB in the mail. I wonder if I’ll ever get anything. Could we move forward in some other way?

ME: Do you possibly have electronic-only EOBs enabled? Can you login to an account with your insurance and look at your claims?

PATIENT: Good thoughts. I do have access to my online account and there is an EOB in there! I attached it. There’s not much more in there, unfortunately. What can I do to help this effort?

ME: You may need to call them to get a better reason why it was considered non-covered. Sometimes, they just accidentally call it non-covered and as soon as you try to ask them why, it magically gets fixed immediately. The EOB is good to have if we’re filing an appeal, though, so that can be your proof of a denied claim (one of the three things they’ll probably need to initiate an appeal). I know it’s a hassle, but it’s really helpful to have an actual reason why it is non-covered before trying to submit anything just so we don’t run into the same problem after an appeal.

Someone at your insurer’s customer service department should be able to answer this question: “Why was CPT Code 93880 considered a non-covered service under my plan?” The process for an appeal denial is pretty much the same no matter what, but we’d give them different content depending on why they claim its non-covered. I hope that helps!

PATIENT: Great, thanks Ryan! I’ll give them a call soon and ask that exact question. I’ll be in touch.

Two Weeks Later (Act 3)

ME: Just an update to let you know BCBS requested all records related to the CIMT service. I just sent them about 20 pages worth of notes your provider thought were relevant, so we’ll see how they respond in about 4 weeks. You should get a long letter in the mail if it is denied again, or a short letter if they approve it. Your letter usually arrives about 2 weeks before ours, so let me know which you get and I can start fixing the new outcome a little sooner.

PATIENT: That’s great! Thank you for staying on top of this, Ryan. I have so much else to do during the day, I’ve been kicking the “call BCBS” can down the road. It sounds like they’re still in the process of determining whether it should be covered. I appreciate it, as always.

Three Months Later (Act 4)

ME: Have you heard anything yet? I received a appeal denial saying it was duplicate (meaning they didn’t change their mind about it being non-covered) a few weeks ago, but nothing else. Did you happen to get a full explanation of the appeal’s denial? Thanks!

PATIENT: Huh… you know, I never received anything more in the mail, and I never checked back up on my dashboard. I’m doing that now…Okay, done looking it up. It does look like I have 2 outstanding claims and I owe ~$200, but that seems lower than I recall it being. Both are for “Vascular Study.” Let me know if there’s any more info I can get you. I should probably pay this dang claim if I haven’t already.

ME: That kind of confirms what I got – just hoping for better news from you. I’ll send you an invoice so you can use your flex card to pay the balance. Thanks for the reply!

Last year, I wrote a comparison between the two options available to state employees through the NC State Health Plan to help people understand the differences between the plans and hopefully make a better decision when selecting a plan for their family. I’m updating that article for to include the changes for the 2019 NC State Health Plan here.

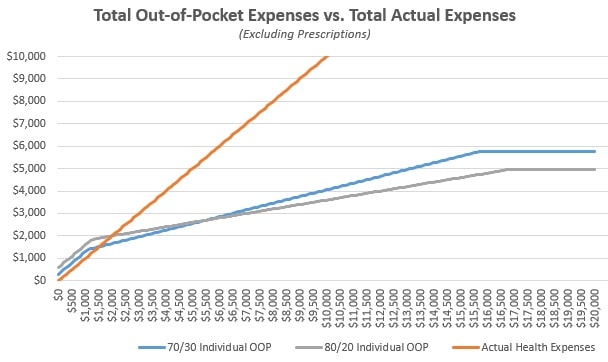

For the 2019 benefit period, North Carolina state employees have two possible choices for their health insurance plan: 70/30 and 80/20.

This article will cover the differences between the two plans and identify the types of families that would benefit from each option. I think the NC State Health Plan is one of the best health insurances you can have in North Carolina, so you are already somewhat ahead of the game with either option. However, because the two plans offer very different benefits, there is usually a “better” choice for everyone and the difference could be significant.

The plan did not actually change much for 2019, so I’ve essentially re-used most of my article from last year and updated it to include the new numbers. I hope this helps!

80/20 vs 70/30 NC State Health Plan Comparison

While most people focus on the cost of their monthly premium, that is not the only factor in your yearly healthcare expense. Sometimes, it makes more sense to pay a higher premium for better coverage if you know that you’re going to need that coverage during the year. Instead, you should try to minimize your total healthcare expense, which includes your premiums, deductibles, copayments, coinsurances, and other out-of-pocket expenses that you’ll have to pay during the year.

This is a direct, side-by-side comparison of the main financial factors that come in to play with these two NC State Health Plan options. While most people focus on the cost of their monthly premium, that is not the only factor in your yearly healthcare expenses. Sometimes, it makes more sense to pay a higher premium for better coverage if you know that you’re going to need that coverage during the year.

Instead of focusing on your premium payment, you should try to minimize your total healthcare expense, which includes your premiums, deductibles, copayments, coinsurances, and other out-of-pocket expenses that you’ll have to pay during the year. There are plenty of exceptions that apply to most situations, but understanding these key terms and aspects of the NC State Health Plan should help you make a reasonable prediction for your costs and set you up to figure out your own unique circumstances.

Below, I have split each of the factors into four basic sections:

Description of the term

The actual specs from each of the two plans

What the difference between the two plans means in concrete terms

And a “math” section that outlines how you can calculate your expected annual expenses using those numbers

Description: Your NC State Health Plan monthly premium is the simplest cost you’ll have to calculate. These are your fixed costs and the amounts you’ll be paying regardless of the real healthcare expenses you’ll have during the year. This number is 100% predictable, it does not change, and it is owed every month, no matter what.

70/30: $25/month ($300/year), or $598/month ($7,176/year)

80/20: $50/month ($600/year), or $720/month ($8,640/year)

Meaning: You can consider these numbers to be the “floor” of your annual health expenses. At the very least, if you have health insurance, you will have to pay your premium. If you never went to the doctor at all, you would have to pay at least $300/$7146 each year to be covered under the 70/30 plan.

Math: Multiply your premium by 12 months to get your annual expense.

Description: This is a flat rate, one-time expense that you incur with every visit to a medical provider for almost any reason. If you visit a PCP or specialist, expect to pay at least this much for your appointment.

70/30: $40 for Primary Care Provider; $100 for Urgent Care; $94 for a Specialist

80/20: $10 for Selected PCP or $25 for Any PCP; $70 for Urgent Care; $80 for a Specialist (a $35 increase from $45 in 2018)

Meaning: Try to predict how many times you’ll need to visit the doctor in a year and consider how much you will save from the difference in the copayment amounts. If you have been seeing the same doctor for a few years, they may be able to help you predict your expected number of visits and let you know what your provider’s plan for the next year might include.

Math: The 80/20 NC State Health Plan will save you $30 per visit to a PCP, $30 per visit to an Urgent Care, and $14 per visit to a specialist. Multiply your expected number of visits to each type of provider to figure out how much money you’ll save on your copayments by choosing to upgrade to the 80/20 plan.

Description: This is a variable rate that only applies after your deductible has been met. After you have met your deductible, you will owe this percentage of all health expenses incurred until you meet your annual out-of-pocket maximum.

A better way to think of the deductible/coinsurance relationship is to consider two periods: before you meet the deductible, and after you have met the deductible. Before, your coinsurance is effectively 100%, because you pay for everything. After, your coinsurance gets reduced to either 20% or 30%.

70/30: 30%

80/20: 20%

Meaning: If these plans were sold at a retail store, you might see this advertisement: “Buy $1,080 worth of healthcare and get your next $4,388 in purchases at 70% to 80% off!” After the plans reach their deductibles and coinsurance begins to apply, you’ll pay significantly less for every bill the rest of the year. Because you are paying more for the fixed cost of the higher premium, you’ll need to pass this point before the 80/20 plan eventually catches back up with the 70/30 plan for total expected expenses.

Math: Try to predict how many times you’ll need to visit the doctor in a year and consider how much you will save from the difference in the copayment amounts. If you have been seeing the same doctor for a few years, they may be able to help you predict your expected number of visits and let you know what your provider’s plan for the next year might include.

A decent estimate for visit costs would be $100 for a PCP visit, $200 for an Urgent Care visit, $300 for a Specialist visit, $500 for a MRI/CT, $2000 for an outpatient ER visit, and $5000 for an inpatient ER visit, per day. The 80/20 NC State Health Plan will save you 10% after your deductible, so you can add up the totals for however many of those services you’re expecting to use and discount 10% for the 80/20 plan to calculate your total savings.

Description: This is the amount in health expenses you’ll have to pay for before your insurance starts paying for the services you receive. Consider this a yearly down payment on your future care, to be paid as you go when necessary.

70/30: $1,080 Individual / $3,240 Family

80/20: $1,250 Individual / $3,750 Family

Meaning: Under either plan, you are on the hook for at least the first $1,080 in health expenses each year, with another $170 added under the 80/20. There are differences in copayments and prescriptions that mean the 80/20 plan will save you money in other ways during the year, but this will become a factor if you receive any of the wide variety of services that fall under your deductible.

Math: Once you know which services will be applied to your deductible, the cost calculation simply 100% of the cost until you’ve met your deductible. After your deductible has been met, your coinsurance will begin to apply.

I think the difference between the way out-of-pocket maximums are calculated carries one of the most important distinctions between the two plans, so I’m giving it a special section.

On the 80/20 plan, there is an “out-of-pocket maximum” of $4,890 for an individual (was $6,850 in 2018) and $14,670 (was $14,300 in 2018) for a family. This is the total amount of money, not including your premiums, that you would possibly ever have to pay for your healthcare in a single year. Even if you were in the hospital from January to December, this is the most you’d have to pay on the 80/20 plan (see assumptions).

However, on the 70/30 plan, there is no “out-of-pocket maximum.” Instead, the 70/30 plan has a cap on the “coinsurance maximum” at a $4,388 / $13,164 rate. Since we just covered how both plans have a deductible and the coinsurance applies to expenses after the deductible, you would think these would just be interchangeable terms. In a kind of sneaky way, this is slipped in as the biggest single category of expense for people who do end up meeting their maximums. Why?

Calling something an “out-of-pocket maximum” means it includes all deductibles and copayments. Literally, everything that the patient must pay for is included in that amount. When it is termed a “coinsurance maximum,” that very specifically applies only to patient responsibilities that are deemed coinsurance; deductibles and copayments are not included in this total.

Basically, you can interpret this to mean that the 80/20 plan only has a $3,640 “after deductible” coinsurance maximum that includes pharmacy benefits, while the 70/30 plan has a $1,080 medical deductible, $3,360 pharmacy deductible, and $4,388 coinsurance maximum separately. While the final out-of-pocket expenses are similar, the methods they each use to get there accumulate at different rates. Depending on where you fall on your expected usage, one side could still make a substantial difference.

Prescription Coverage

There are too many possible variables to really give a simple, universal estimate for prescription expenses, but I can at least guide you on how to figure out your own costs. It is easy to calculate the minimum ($0, because you don’t use prescriptions) or the maximum ($2,500/$3,360 when you reach your pharmacy maximum) expense, but everything in between is pretty much situational. To calculate your expected prescription costs per year, follow these steps:

Make a list of your medications. All of them, even over-the-counter meds and the ones you forget to take.

Look up every medication on your formulary. This is the document where you can find your drug’s “tier,” a hierarchical cost-based categorization system that the NC State Health Plan uses to decide how much you’ll pay for each drug. If you cannot find the drug, you will need to contact your insurer directly to ask about a more specific medication than they have listed in the general formulary. Estimate retail value for over-the-counter medications.

There are additional pharmacy resources linked at the bottom of this page.

Multiply the number of refills you’ll need by the copayments / out-of-pocket expense for each tier. You pay more for higher tier medications, so taking lower tiered or generic medications could potentially save a lot of money each year.

This is a somewhat oversimplified method, but it should give you a good starting point. There are a few other ways to reduce your costs:

If you take a Tier 2 or Tier 3 drug, contact your provider to see if a Tier 1 drug might be a suitable alternative. This may require an appointment or additional lab work, so take that extra cost into consideration.

If you expect to be taking the medication for at least the next three months, you may be able to get a cheaper, 90-day supply by using a mail order pharmacy.

If you don’t use GoodRx.com, sign up. We have discount cards at our office and would be glad to share – they send 1,000 of them every 3 months and we have way too many. Please, take them. I’ll give you 10, just in case you lose nine of them. Regardless of your insurance coverage, this site helps you find the best prices at different pharmacies and can save you hundreds of dollars on most non-formulary medications.

Necessary Details of the NC State Health Plan

This information should give you a good starting point for predicting your coverage, but it is not comprehensive. These are other categories of health expenses that you need to be aware of and factor in to your own personal calculations.

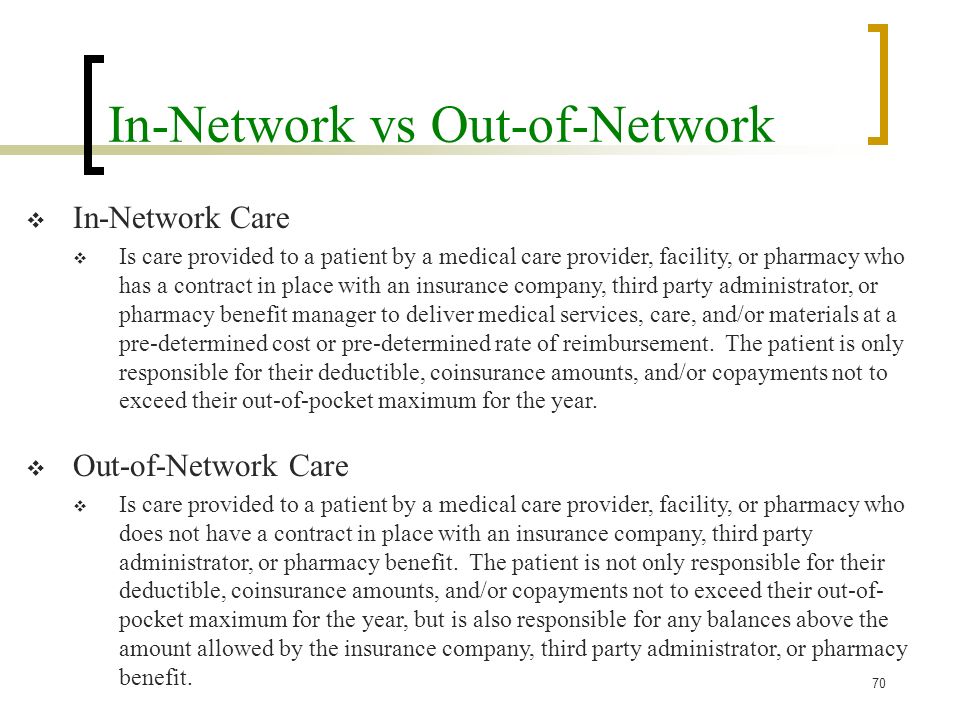

Out-of-network expenses. Visits to an out-of-network provider are “covered” under a separate set of benefits from your in-network out-of-pocket expenses. These benefits are usually at least 50% worse and there are a lot more things that are denied or non-covered, so it is best to stay in-network for almost anything you do.

The number of people covered in the Family plan. The “Subscriber + Family” option covers one kid, two kids, ten kids, or as many kids as you want to have. No matter how many kids are included, the Family Maximums are the same. If you consider the smallest “Family” to be 3 people, the price per person gets reduced significantly with every additional child.

3 people; $14,670 maximum = $4,890 / person, maximum

4 people; $14,670 maximum = $3,667 / person, maximum

5 people; $14,670 maximum = $2,934 / person, maximum

The amount of work you are willing to do. This especially applies to prescription coverage. Some of the most effective ways to save money will require you to call your insurer, fill out forms, document everything, track of receipts, and/or generally make you deal with your insurer’s customer service department. Assess how likely you are to make that effort, if needed.

Unexpected Expenses. You might get lucky, but remember that you are trying to predict 2019 health expenses for your entire family in October 2018. Things can change in the next hour, much less 2-14 months from now. If you choose the 70/30 plan, figure out how comfortable you are with having an accident and meeting the maximum, then consider that additional risk when selecting a plan.

Other NC State Health Plan Notes & Considerations

The “Free” Annual Wellness Visit is not included in the 70/30’s benefits, so your annual physical will have a $40 copayment just like any other visit. The 80/20 plan covers this at 100%.

For the 80/20 plan, Tier 3 drugs are applied to your normal deductible and coinsurance, instead of having a set copayment. While this probably makes the drug more expensive, having more expenses applied to a deductible is always a good thing for people who expect to hit their maximums. You could end up owing the pharmacy a lot of money early in the year, but then owe much less for all other health expenses combined for the rest of the year.

The 70/30 doesn’t cover ACA Preventive Medicines, either. Basically, you should just expect to pay more for birth control with the 70/30 plan, especially for branded medications.

Emergency room copayments are only a $37 difference, but the big part is in the 20% vs. 30% coinsurance owed. 10% of a single ER visit adds up quickly, so expect to pay at least $500-$1000 more for a single night’s ER stay with the 70/30 plan.

Your coinsurance kicks in sooner under the 70/30 plan ($170/$510 sooner for an individual/family plan), but your coinsurance rate is slightly worse. Because the 80/20 plan “catches up” with the 70/30 at a 10% rate, it would take $1,700/$5,100 in additional health expenses under each plan to reach a break-even point where you’ve paid the same amount in “deductible + coinsurance” under either plan.

The individual deductible on the 80/20 plan was reduced by $1,960, which is good news for everyone, but especially single employees with no dependents and families where one person generally uses most of the healthcare dollars on the plan.

Actions You Need To Take

It probably won’t be fun, but you still need to do this stuff.

Elect Your Plan. Kind of a weird way to say, “Choose a Plan,” but I guess we’ll go with calling it an election! You must choose the 80/20 or 70/30 plan. If you don’t make a choice, you will get defaulted to 70/30 and be charged an extra fee for the 70/30 plan for not making a choice.

Complete the Tobacco Attestation Credit. Even if you did it last year, you need to do it again. This saves you $60/month on your NC State Health Plan premium under every option.

Select a Primary Care Provider. There is a new link on the left side of your NC State Health Plan online account that allows you to change your PCP in just a few clicks. It was never too difficult to do over the phone, but any saved phone call to BCBS is a step in the right direction. We hope you choose Family Care!

Review Your Dependent Information. If applicable, make sure your spouse and kid(s) are enrolled on your plan. If you were married or had a kid since last enrollment, congratulations! Now make sure they are still on your plan! Double check that BCBS has demographic information like date of birth, mailing address, and phone numbers correct, as those can be a big hassle to correct later.

Print A Confirmation Statement. This is probably the most important thing you’ll do for yourself, so don’t skip this. I have heard so many nightmare stories and have listened to dozens of patients complain about being enrolled in the wrong plan on accident, and the only ones that I’ve seen win are the patients with their own receipts and records. Do not trust BCBS to get your information correct. Stay on top of it yourself and don’t let them make a mistake that costs you coverage, money, and sanity.

Summary

As with everything in healthcare, the standard “subject to individual determination” disclaimers always apply and nobody will, or should, give you a definite answer. I cannot tell you which plan you should choose, but I think you can use this guide to make that decision on your own.

All you can do is make the best estimate possible with the information you have at the time. Someone telling you they can accurately predict your actual health expenses is either lying, inexperienced, or delusional. Be ready to adjust if something does happen with your health and you need more extensive care than planned. Factor that potential into your decision and always be prepared for the worst-case scenario. I’ve found it is always better to be relieved things weren’t as bad as you thought, rather than being mad that they were worse.

For most people, your realized benefits under either plan will always be within a few hundred dollars of the other, so don’t stress out about the decision too much. This decision is not going to bankrupt you if you make the wrong choice. Either way, you will still have a plan that is better and cheaper than anything you could get on the individual marketplace.

Thank you for reading! I hope this helps you decide. Contact Ryan if you have any questions!

Good luck!

Assumptions

During the article, I left out mentioning many of the exceptions and individual circumstances that are possible with the NC State Health Plan. The article was already 3300 words, so I thought I’d save the trouble. Here are a few assumptions I made for all of the pricing and cost examples.

This is a breakdown of the distinct categories of expenses that you’ll have under either plan. Since it would be a little too confusing to talk about each of the 16 possible choices, I’m only using the “Subscriber Only” and “Subscriber + Family” plans as the low/high-end examples. You should adjust the numbers slightly if you choose the “Subscriber + Child(ren)” or “Subscriber + Spouse” options.

These numbers also assume that you will complete the Tobacco Attestation document and save $60/month on your premiums. If not, you should expect to pay an extra $720/year in premiums, but the rest of the expense calculations should remain the same.

I am also assuming you use a Blue Options Designated Specialist, visit your Selected Primary Care Provider for primary care services, and only visit in-network providers for all your healthcare needs. If you seek services under any other designations, you should expect to pay more.

Last year, I wrote a comparison between the three 2017 North Carolina State Health Plan options available to state employees to help people understand the differences between the plans and hopefully make a better decision when selecting a plan for their family. The State Health Plan (NCSHP) makes up our largest group of patients and I know it helped at least one person, so I figured it might be helpful to do the same thing this year. The information in last year’s article is still worth checking out if you are new to health insurance, in general, but this year should be a bit simpler.

Because the state eliminated the popular CDHP option for 2018 enrollment, NC state employees are left with only two possible choices: 70/30 and 80/20.

The rest of this article will cover the differences between the two plans and identify the types of families that would benefit from each option. I think the NC State Health Plan is one of the best health insurances you can have in North Carolina, so you are already somewhat ahead of the game with either option. However, because the two plans offer different benefit structures, there is usually a “better” choice for everyone.

80/20 vs 70/30 State Health Plan Comparison

This is a direct, side-by-side comparison of the main financial factors that come in to play with these two health insurance plans. While most people focus on the cost of their monthly premium, that is not the only factor in your yearly healthcare expenses. Sometimes, it makes more sense to pay a higher premium for better coverage if you know that you’re going to need that coverage during the year.

Instead of focusing on your premium payment, you should try to minimize your total healthcare expense, which includes your premiums, deductibles, copayments, coinsurances, and other out-of-pocket expenses that you’ll have to pay during the year. There are plenty of exceptions that apply to most situations, but understanding these key terms and aspects of your plan should help you make a reasonable prediction for your costs and set you up to figure out your own unique circumstances.

Below, I have split each of the factors into four basic sections:

Description of the term

The actual specs from each of the two plans

What the difference between the two plans means in concrete terms

And a “math” section that outlines how you can calculate your expected annual expenses using those numbers

Description: Your monthly premium is the simplest cost you’ll have to calculate. These are your fixed costs and the amounts you’ll be paying regardless of the real healthcare expenses you’ll have during the year. This number is 100% predictable, it does not change, and it is owed every month, no matter what.

70/30: $25/month ($300/year), or $598/month ($7,176/year)

80/20: $50/month ($600/year), or $720/month ($8,640/year)

Meaning: You can consider these numbers to be the “floor” of your annual health expenses. At the very least, if you have health insurance, you will have to pay your premium. If you never went to the doctor at all, you would have to pay at least $300/$7146 each year to be covered under the 70/30 plan. While the $720/month maximum premium seems steep, I would encourage you to try shopping for a plan on the individual marketplace and see exactly what kind of value you’re getting on the plan. The difference will probably be surprising. These premiums are very reasonable when compared with other options, especially considering the quality of the benefits of the plan.

Math: Multiply your premium by 12 months to get your annual expense.

Description: This is a flat rate, one-time expense that you incur with every visit to a medical provider for almost any reason. If you visit a PCP or specialist, expect to pay at least this much for your appointment.

70/30: $40 for primary doctor, $94 for a specialist

80/20: $10 for primary doctor (Need to visit Selected PCP); $45 for a Blue Options Designated specialist

Meaning: Try to predict how many times you’ll need to visit the doctor in a year and consider how much you will save from the difference in the copayment amounts. If you have been seeing the same doctor for a few years, they may be able to help you predict your expected number of visits and let you know what your provider’s plan for the next year might include.

Math: The 80/20 plan will save you $30 per visit to a PCP, $30 per visit to an Urgent Care, and $49 per visit to a specialist. Multiply your expected number of visits to each type of provider to figure out how much money you’ll save on your copayments by choosing to upgrade to the 80/20 plan.

Description: This is a variable rate that only applies after your deductible has been met. After you have met your deductible, you will owe this percentage of all health expenses incurred until you meet your annual out-of-pocket maximum.

A better way to think of the deductible/coinsurance relationship is to consider two periods: before you meet the deductible, and after you have met the deductible. Before, your coinsurance is effectively 100%, because you pay for everything. After, your coinsurance gets reduced to either 20% or 30%.

70/30: 30%

80/20: 20%

Meaning: If these plans were sold at a retail store, you might see this advertisement: “Buy $1,080 worth of healthcare and get your next $4,388 in purchases at 70% to 80% off!” After the plans reach their deductibles and coinsurance begins to apply, you’ll pay significantly less for every bill the rest of the year. Because you are paying more for the fixed cost of the higher premium, you’ll need to incur at least $1,700 in expenses AFTER you have reached your deductible before the 80/20 plan eventually catches back up with the 70/30 plan for total expected expenses.

Math: Try to predict how many times you’ll need to visit the doctor in a year and consider how much you will save from the difference in the copayment amounts. If you have been seeing the same doctor for a few years, they may be able to help you predict your expected number of visits and let you know what your provider’s plan for the next year might include.

A decent estimate for visit costs would be $100 for a PCP visit, $200 for an Urgent Care visit, $300 for a Specialist visit, $500 for a MRI/CT, $2000 for an outpatient ER visit, and $5000 for an inpatient ER visit, per day. The 80/20 plan will save you 10% after your deductible, so you can add up the totals for however many of those services you’re expecting to use and discount 10% for the 80/20 plan to calculate your total savings.

Description: This is the amount in health expenses you’ll have to pay for before your insurance starts paying for the services you receive. Consider this a yearly down payment on your future care, to be paid as you go when necessary.

70/30: $1,080 Individual / $3,240 Family

80/20: $1,250 Individual / $3,750 Family

Meaning: Under either plan, you are on the hook for at least the first $1,080 in health expenses each year, with another $170 added under the 80/20. There are differences in copayments and prescriptions that mean the 80/20 plan will save you money in other ways during the year, but this will become a factor if you receive any of the wide variety of services that fall under your deductible.

Math: Once you know which services will be applied to your deductible, the cost calculation simply 100% of the cost until you’ve met your deductible. After your deductible has been met, your coinsurance will begin to apply.

I think the difference between the way out-of-pocket maximums are calculated carries one of the most important distinctions between the two plans, so I’m giving it a special section.

On the 80/20 State Health Plan plan, there is an “out-of-pocket maximum” of $6,850 for an individual and $14,300 for a family. This is the total amount of money, not including your premiums, that you would possibly ever have to pay for your healthcare in a single year. Even if you were in the hospital from January to December, this is the most you’d have to pay on the 80/20 plan (see assumptions).

However, on the 70/30 State Health Plan, there is no “out-of-pocket maximum.” Instead, the 70/30 plan has a cap on the “coinsurance maximum” at a $4,388 / $13,164 rate. Since we just covered how both plans have a deductible and the coinsurance applies to expenses after the deductible, you would think these would just be interchangeable terms. In a kind of sneaky way, this is slipped in as the biggest single category of expense for people who do end up meeting their maximums. Why?

Calling something an “out-of-pocket maximum” means it includes all deductibles and copayments. Literally, everything that the patient must pay for is included in that amount. When it is termed a “coinsurance maximum,” that very specifically applies only to patient responsibilities that are deemed coinsurance; deductibles and copayments are not included in this total.

Basically, you can interpret this to mean that the 80/20 plan only has a $5,600 “after deductible” coinsurance maximum that includes pharmacy benefits, while the 70/30 plan has a $1,080 medical deductible, $3,360 pharmacy deductible, and $4,388 coinsurance maximum separately. While the final out-of-pocket expenses are similar, the methods they each use to get there accumulate at different rates. Depending on where you fall on your expected usage, one side could still make a substantial difference.

Prescription Coverage

There are too many possible variables to really give a simple, universal estimate for prescription expenses, but I can at least guide you on how to figure out your own costs. It is easy to calculate the minimum ($0, because you don’t use prescriptions) or the maximum ($2,500/$3,360 when you reach your pharmacy maximum) expense, but everything in between is pretty much situational. To calculate your expected prescription costs per year, follow these steps:

Make a list of your medications. All of them, even over-the-counter meds and the ones you forget to take.

Look up every medication on your formulary. This is the document where you can find your drug’s “tier,” a hierarchical cost-based categorization system that your insurer uses to decide how much you’ll pay for each drug. If you cannot find the drug, you will need to contact your insurer directly to ask about a more specific medication than they have listed in the general formulary. Estimate retail value for over-the-counter medications.

There are additional pharmacy resources linked at the bottom of this page.

Multiply the number of refills you’ll need by the copayments / out-of-pocket expense for each tier. You pay more for higher tier medications, so taking lower tiered or generic medications could potentially save a lot of money each year.

This is a somewhat oversimplified method, but it should give you a good starting point. There are a few other ways to reduce your costs:

If you take a Tier 2 or Tier 3 drug, contact your provider to see if a Tier 1 drug might be a suitable alternative. This may require an appointment or additional lab work, so take that extra cost into consideration.

If you expect to be taking the medication for at least the next three months, you may be able to get a cheaper, 90-day supply by using a mail order pharmacy.

If you don’t use GoodRx.com, sign up. We have discount cards at our office and would be glad to share – they send 1,000 of them every 3 months and we have way too many. Please, take them. I’ll give you 10, just in case you lose nine of them. Regardless of your insurance coverage, this site helps you find the best prices at different pharmacies and can save you hundreds of dollars on most non-formulary medications.

This information should give you a good starting point for predicting your coverage, but it is not comprehensive. These are other categories of health expenses that you need to be aware of and factor in to your own personal calculations when deciding on one of the State Health Plan options.

Out-of-network expenses. Visits to an out-of-network provider are “covered” under a separate set of State Health Plan benefits from your in-network out-of-pocket expenses. These benefits are usually at least 50% worse and there are a lot more things that are denied or non-covered, so it is best to stay in-network for almost anything you do.

The number of people covered in the Family plan. The “Subscriber + Family” option covers one kid, two kids, ten kids, or as many kids as you want to have. No matter how many kids are included, the Family Maximums are the same. If you consider the smallest “Family” to be 3 people, the price per person gets reduced significantly with every additional child.

3 people; $14,300 maximum = $4,766 / person, maximum

4 people; $14,300 maximum = $3,575 / person, maximum

5 people; $14,300 maximum = $2,860 / person, maximum

etc.

The amount of work you are willing to do. This especially applies to prescription coverage. Some of the most effective ways to save money will require you to call your insurer, fill out forms, document everything, track of receipts, and/or generally make you deal with your insurer’s customer service department. Assess how likely you are to make that effort, if needed.

Unexpected Expenses. You might get lucky, but remember that you are trying to predict 2018 health expenses for your entire family in October 2017. Things can change in the next hour, much less 2-14 months from now. If you choose the 70/30 plan, figure out how comfortable you are with having an accident and meeting the maximum, then consider that additional risk when selecting a plan.

Other State Health Plan Notes & Considerations

The state removed the “Free” Annual Wellness Visit from the State Health Plan 70/30 benefits, so your annual physical will have a $40 copayment just like any other visit. Last year, this visit to cover recommended preventive screenings and testing was covered 100% for all plans.

For the 80/20 plan, Tier 3 drugs are applied to your normal deductible and coinsurance, instead of having a set copayment. While this probably makes the drug more expensive, having more expenses applied to a deductible is always a good thing for people who expect to hit their maximums. You could end up owing the pharmacy a lot of money early in the year, but then owe much less for all other health expenses combined for the rest of the year.

The 70/30 doesn’t cover ACA Preventive Medicines, either. I am unsure how that law is being implemented or supported right now, but basically you should just expect to pay more for birth control with the 70/30 plan, especially for branded medications.

Emergency room copayments are only a $37 difference, but the big part is in the 20% vs. 30% coinsurance owed. A 10% difference in the bill from a single ER visit adds up quickly, so you should really expect to pay at least $500-$1000 more for a single night’s ER stay with the 70/30 plan in you have not yet met your deductible.

Your coinsurance kicks in sooner under the 70/30 plan ($170/$510 sooner for an individual/family plan), but your coinsurance rate is slightly worse. Because the 80/20 State Health Plan “catches up” with the 70/30 at a 10% rate, it would take $1,700/$5,100 in additional health expenses under each plan to reach a break-even point where you’ve paid the same amount in “deductible + coinsurance” under either plan.

If most of your health expenses come from prescriptions, the 80/20 plan will save you $860 between the $2,500 and $3,360 level. However, the advantage changes if you have more than one person in your family with high cost prescriptions. Under the 70/30 plan, the individual and family have the same $3,360 deductible, while the 80/20 plan has a $4,000 family maximum. If more than one person expects to spend ~$2,000 or more on prescriptions, the 70/30 plan will save you an extra $640 on those medications.

Actions You Need To Take

It probably won’t be fun, but you still need to do this stuff.

Elect Your Plan. Kind of a weird way to say, “Choose a Plan,” but I guess we’ll go with calling it an election! You must choose the 80/20 or 70/30 plan. If you don’t make a choice, you will get defaulted to 70/30 and be charged an extra fee for the 70/30 plan for not making a choice.

Complete the Tobacco Attestation Credit. Even if you did it last year, you need to do it again. This saves you $60/month on your State Health Plan premium under every option.

Select a Primary Care Provider. There is a new link on the left side of your NC State Health Plan online account that allows you to change your PCP in just a few clicks. It was never too difficult to do over the phone, but any saved phone call to BCBS is a step in the right direction. We hope you choose Family Care!

Review Your Dependent Information. If applicable, make sure your spouse and kid(s) are enrolled on your plan. If you were married or had a kid since last enrollment, congratulations! Now make sure they are still on your plan! Double check that BCBS has demographic information like date of birth, mailing address, and phone numbers correct, as those can be a big hassle to correct later.

Print A Confirmation Statement. This is probably the most important thing you’ll do for yourself, so don’t skip this. I have heard so many nightmare stories and have listened to dozens of patients complain about being enrolled in the wrong plan on accident, and the only ones that I’ve seen win are the patients with their own receipts and records. Do not trust BCBS to get your information correct. Stay on top of it yourself and don’t let them make a mistake that costs you coverage, money, and sanity.

Summary

As with everything in healthcare, the standard “subject to individual determination” disclaimers always apply and nobody will, or should, give you a definite answer. My wife is a state employee and I am making this same decision for my family, so you can consider this my way of talking out the decision for myself. I cannot tell you which plan you should choose, but I think you can use this guide to make that decision on your own.

All you can do is make the best estimate possible with the information you have at the time. Someone telling you they can precisely predict your actual health expenses is either lying, inexperienced, or delusional. Be ready to adjust if something does happen with your health and you need more extensive care than planned. Factor that potential into your decision and always be prepared for the worst-case scenario. I’ve found it is always better to be relieved things weren’t as bad as you thought, rather than being mad that they were worse.

For most people, your realized benefits under either plan will always be within a few hundred dollars of the other, so don’t stress out about the decision too much. This decision is not going to bankrupt you if you make the wrong choice. Either way, you will still have a plan that is better and cheaper than anything you could get on the individual marketplace.

Thank you for reading! I hope this helps you decide. Contact Ryan if you have any questions!

Good luck!

Assumptions

During the article, I left out mentioning many of the exceptions and individual circumstances that are possible with the NC State Health Plan. The article was already 3300 words, so I thought I’d save the trouble. Here are a few assumptions I made for all of the pricing and cost examples.

This is a breakdown of the distinct categories of expenses that you’ll have under either plan. Since it would be a little too confusing to talk about each of the 16 possible choices, I’m only using the “Subscriber Only” and “Subscriber + Family” plans as the low/high-end examples. You should adjust the numbers slightly if you choose the “Subscriber + Child(ren)” or “Subscriber + Spouse” options.

These numbers also assume that you will complete the Tobacco Attestation document and save $60/month on your premiums. If not, you should expect to pay an extra $720/year in premiums, but the rest of the expense calculations should remain the same.

I am also assuming you use a Blue Options Designated Specialist, visit your Selected Primary Care Provider for primary care services, and only visit in-network providers for all your healthcare needs. If you seek services under any other designations, you should expect to pay more.

How do I know if I am being billed the correct amount for my visit?

As most people can understand, figuring out exactly how much a particular medical service will cost can be extremely difficult. There are a lot of variables that factor in to the final cost of any care you receive, but it is still possible to get pretty solid information and set reasonable expectations for the most common types of services you will encounter. This post is designed to help you understand the basics of the billing process to help you identify any problems and know learn how to fix them.

When you are billed by any medical provider, they are usually working with the best possible information they can get about your insurance coverage at the time of service. However, regardless of how well they might be able to predict your coverage, providers are often still sometimes just as surprised as the patient when dealing with unexpected changes in coverage and quirks with different insurance plans. Because of this uncertainty, the amount you pay at the time of service may differ from the amount you actually owe.

No matter how much your provider may try to help navigate your insurance policy, the ultimate responsibility for the balance of a denied claim belongs to the patient. The total amount you will owe is called “patient responsibility” because you’re the one who will have to pay the bill and ultimately responsible for ensuring that you are paying the correct amount. Billing errors aren’t common, but they do happen and can be fixed pretty easily if you know how to find them.

PATIENT RESPONSIBILITY

There are three things that you’ll need to keep track of to know for sure if you are being billed the correct amount by your provider.

The amount you paid at the time of service.

The amount your explanation of benefits stated you would owe.

The amount of the bill you receive from your provider.

Ideally, #1 and #2 are equal and #3 never happens because you’ve already paid the correct amount for the service you’ve received after the appointment. For standard visits and simple insurance plans with copayments instead of deductibles, this is usually pretty easy. Your insurance says you’ll owe $25 for a visit, so you’ll pay your $25 when you check out and know that the rest will be covered. Easy. Unfortunately, there are far more instances where deductibles, co-insurances, exclusions, and other insurance hurdles will also apply to your benefits and make things more difficult to predict.

These types of “high deductible / shared percentage” plans are becoming much more common and make up all of the possible options available on the health exchange for Durham County in 2017. Because the total bills you’ll receive for these kind of plans are very much dependent on factors that you can’t guarantee before the service is rendered, the amounts you are charged for certain services are much more unpredictable.

This is where a basic checklist comes in handy:

#1. Remember what you paid.

Because most FSA plans now allow you to submit an electronic PDF of your receipts for tax purposes, you probably don’t need to save a real paper receipt of your transaction. However, you will still need to keep track of how much you’ve paid, just like any other bill you might have. You can also always refer back to your credit card statement or look at your online banking history to reference the charges, if needed. Either way, if you actually get a bill, you’ll want to look up previous payments towards your expected out-of-pocket expenses for that service and make sure they are already deducted from your total balance.

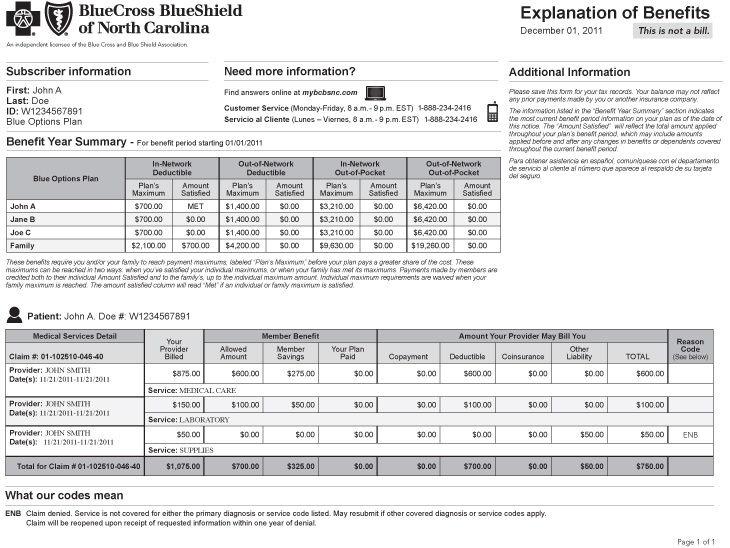

#2. Check your Explanation of Benefits (EOB).

This is a statement issued by your insurance company and either mailed or uploaded to your online member services account about 2-3 weeks after every claim filed on your behalf by a medical provider or facility. Your final out-of-pocket expenses are usually listed under a column titled “total patient responsibility” and will your insurer’s reasoning for each balance owed will be detailed on this document after your insurance benefits have been assigned to your claim. If you receive a bill because your insurer says your plan didn’t pay for something, this document will tell you why.

#3. Check your bill.

If you know what you’ve paid (shown on your receipt) and how much you should owe (based on your EOB), you can pretty much figure out how much you’ll be billed after the service.

Amount owed on EOB – Amount paid at time of service = Amount still owed

There are always exceptions at each facility you visit that may lead to separate fees associated with their services, but those are usually relatively minor compared to the total cost of care. If you think there is a problem with the amount you are being billed, be sure to contact your provider and double check to see if there are any other fees or balances that may have contributed to the difference before attempting to contact your insurance.

FIXING A PROBLEM

So, you’ve looked at your EOB and examined at your bill and the two numbers still don’t match up. Or, worse, they do matchup and the amount is significantly higher than you were expecting. Now that you have identified a potential discrepancy with the bill, what do you do about it? Your first phone call depends on where you find the problem.

My EOB and the bill from my provider both show the same amount due.

This is a problem between you and your insurer. In this case, the problem would be that you disagree with the amount your insurer said you would owe since your provider’s information matches the insurer. This means that the problem lies at the start of the claim process where your insurance assigned your plan’s benefits to the claim they received. You thought you would owe one thing, but your insurance said something else.

Here are the steps you should take to work towards a solution:

On your EOB, look up the “Remark Code” for the line items that are being denied. These are generally 2 or 3 digit alphanumeric codes that reference a longer explanation of denial later on in the document. This is a summary of the actual reason your insurance is using to deny this charge. If this summary explanation does not make sense to you based on how you understand your policy, you can call your insurance company for a full explanation.

When you call customer service, be sure to have your insurance card and EOB in front of you so you can reference the date of service, amount billed, and the specific line item that you are questioning. They will be able to look up your insurance policy and re-examine the specific claim you are referencing at the same time to make sure your plan’s benefits were applied correctly.

If your benefits were applied correctly, the representative can answer questions about your plan and help you understand how your benefits will be applied in the future so you can possibly avoid the same situation next time. Sometimes, payment is denied because they need to update information about your insurance plan, so you can answer their questions over the phone and take care of the balance in just a couple minutes. Learning more about your policy and how your insurance will process a similar claim could make a big difference in the long run.

If your benefits were not applied correctly, the customer service representative should be able to notice the mistake and submit your claim for reprocessing. If this happens to be the case, you’ll want to get a reference number for the call and notify the provider that sent you a bill. The insurance will likely give you a quote like “we will reprocess this claim and send a corrected claim to your provider in 2-3 weeks.” Whenever they give you a timeframe, double it and then call your provider back to see if everything has been resolved.

My EOB says one amount owed, but the provider’s bill says something different.

If you have carefully looked at your receipt, EOB, and billing statement and still think there is a problem that is unrelated to how your insurance processed the claim, here are several logical explanations, in order of potential likelihood:

You owed money for another claim. Most of the time, your billing statement only includes claim details for the claims with a balance owed. It is possible that your provider applied part of a payment you’d made to a claim that is not currently on your billing statement because that balance was covered.

You paid $100 at the time of service, but $40 went towards a balance from January and $60 went towards a balance from April. Because you also owed $100 from the April visit, you may receive a bill for $40 for that claim even though you paid $100 already.

You owed money for additional fees and services not on the bill. Every practice is different, but there are always additional fees that you may have to pay for services that are not reimbursable by insurance companies. These include charges for things like missed appointments, form completion, records requests, and certain lab tests that aren’t covered by insurances. Part of a payment you made may have been applied to one of these types of charges.

You had a previous credit applied. Sometimes, the system actually works in your favor and you might overpay for a charge up front. When this happens, you’ll receive a credit on your account that may be applied to future balances and reduce the amount you are charged at the time of service. If you were unaware of the credit, you may have expected a service to be cheaper than you thought when you paid.

You overpaid by $20 a couple months ago, so your provider only charged you $5 for your usual $25 copayment. When you look at your EOB, it shows that you would owe $25 for that visit, even if you only paid $5 that day.

There was a mistake. Most financial correspondence between your insurer and provider is electronic and automated, but that doesn’t mean there aren’t mistakes. As the provider, we receive batches of claim data that includes dozens of claim rows and about 20 columns of payment information per claim from the insurer and we have to sift through every row, column, and number to ensure its accuracy. As you can imagine, it is very tough to get through this process and end up 100% perfect. Even at 99.9% accuracy, that means an average primary care facility will generate about 10 incorrect patient balances per month. Before getting upset or worried about the possibility of owing for a service, have your provider double check the claim first before attempting to appeal through your insurer.

You can easily identify which one of these situations is likely to apply to you by asking for a “transactional summary” of all your claims for a certain time period. All providers may call this report something different, so you’ll just need to ask for something that shows all the charges on all claims filed by the provider and how all of your payments were applied to your account over a certain time period. This will let you see, line by line, what caused the problem.

Most of the time, any changes to a bill with an amount that differs from your EOB will always be initiated by the provider who performed the service, so it’s best to start at the source if you want to fix a potential problem. I hope this has given you the knowledge to better understand your medical bills and the confidence to discuss them with your provider, if needed.

If you have any questions related to the content of this article or if you’ve experienced any other type of situation that I didn’t address, I’d love to read your comments below. Thanks for reading!

“Why do you wait at your door, woman,

Alone in the night?”

“I am waiting for one who will come, stranger,

To show him a light.

He will see me afar on the road

And be glad at the sight.”

“Have you no fear in your heart, woman,

To stand there alone?

There is comfort for you and kindly content

Beside the hearthstone.”

But she answered, “No rest can I have

Till I welcome my own.”

“Is it far he must travel to-night,

This man of your heart?”

“Strange lands that I know not and pitiless seas

Have kept us apart,

And he travels this night to his home

Without guide, without chart.”

“And has he companions to cheer him?”

“Aye, many,” she said.

“The candles are lighted, the hearthstones are swept,

The fires glow red.

We shall welcome them out of the night—

Our home-coming dead.”

To help all of the State employees of North Carolina figure out which version of the State Health Plan would be best for them during the upcoming year, I thought we would attempt to review the differences between the three options – CDHP (85/15), Enhanced 80/20, and Traditional 70/30. The State has developed a very informative site with lots of details and specifics for the State Health Plan, so I won’t repeat anything you can find there. The goal of this post is to compare, line by line, what the numbers associated with each plan mean and which types of medical situations end up being the preferred option financially for each person once all expenses have been considered.

All State Employees should have received a “Decision Guide for Open Enrollment” packet from their insurer for the 2017 benefit period sometime in the past few weeks. You can use the “2017 State Health Plan Comparison” table on Page 8 in this booklet, or you can click on this link to get the PDF online. Here we go!

2017 North Carolina State Health Plan Comparison

HRA Starting Balance: You’ll notice that the CDHP plan is the only option with an Health Reimbursement Account (HRA). An HRA is basically a fund that your employer sets aside to pay for your qualifying medical expenses. With the CDHP plan, an individual has their first $600 in health expenses paid through their employer’s HRA. This is basically free money, as long as you need it and use it for things that are approved by your plan (eg. doctor’s visits, most prescriptions). Effectively, this splits the CDHP’s $1,500 deductible into two different periods, where you end up only having to pay once you hit $601 in expenses each year.

One thing to consider is that you actually need to use $600 in health expenses for this aspect of the plan to help. If you don’t use it, the $600 set aside for you in your employer’s account usually resets and lets the employer keep any unused funds to help reduce expenses the following year. While $600 is the same to anyone, this is an especially nice feature for people who expect their total health expenses to be less than $600 per year because they’ll never have to pay anything except their premiums.

Annual Deductible: A deductible is the amount of money you will have to pay out-of-pocket for non-preventive services before the actual benefits on your insurance plan will start to take effect. Of the three options available, the 70/30 has the lowest deductible, but that doesn’t mean it is the best plan. This means that the plan’s benefits kick in earlier, but the 70/30 plan also has greater expenses after the deductible and a much higher out-of-pocket maximum than the other plans. Other than just the dollar amount, there are two distinct differences in how these deductibles are applied:

The CDHP plan applies all medical expenses to the deductible. Your sick visits, specialist appointments, prescriptions – everything goes towards your initial $1,500 deductible. Other than the covered ACA Preventive Services, this plan doesn’t pay any of your health care expenses until after you have met the deductible.

The 80/20 and 70/30 plan have co-payments for PCP visits, urgent cares, and prescriptions so the deductible only applies to things like surgeries, labs, and hospital visits. While the deductibles are lower, they are also less likely to be met because they only apply to certain things.

Co-Insurance: You might notice that the co-insurance rate is also indicative of the name of the plan – eg. the 80/20 plan features a 20% co-insurance. The co-insurance is a percentage that requires the patient to pay a certain portion of approved medical services once their deductibles have been met. Basically, as a reward for paying 100% of everything out-of-pocket before you met the deductible, your insurance will now start helping pay your health expenses by reducing your portion to either 15%, 20%, or 30%, depending on the plan. Once you have met your deductible, this is the percentage of your health expenses you will be required to pay until you have met your co-insurance maximum.

Medical Co-Insurance Maximum: The 70/30 plan is the only one that has a medical co-insurance maximum. The other plans have their own maximums, so while this seems like a small bit of semantics, but it actually makes a pretty big difference in your possible expenses. The CDHP only has a combined out-of-pocket maximum that includes co-insurance and pharmacy benefits, while the 80/20 plan skips the co-insurance maximum and separates the out-of-pocket maximums between medical and pharmacy. By calling it a “co-insurance maximum” and not a “out-of-pocket maximum,” this number does not include the annual deductible that has already been paid.

This graphic does not include the separate prescription deductibles associated with the 80/20 and 70/30 plans.

Because the $4,350 out-of-pocket maximum in the 80/20 plan includes the $1,250 deductible, the 80/20 plan’s effective “co-insurance maximum” is really only $3,100. With the 70/30 plan, you’ll be paying the $1,080 deductible PLUS $4,388 more. A small difference, but one that costs over $1,200 if it actually comes into play. Also, it is important to remember that the 80/20 and 70/30 plans have separate deductibles for prescriptions, which we will get into soon.

Medical Out-of Pocket Maximum: As mentioned in the previous paragraph, the medical out-of-pocket maximum includes all out-of-pocket expenses a person would have to pay for medical services each year. This includes co-payments, co-insurances, and deductibles. For the 80/20 plan, this means you’ll have a cap on your medical expenses each year of $4,350. Because this number includes the deductible, you’ll basically be paying a $1,250 deductible, and then +20% of the next $15,500 in health expenses you incur (for a total of $4,350). This number puts a cap on your total annual medical expenses, so you can consider this the limit of a “worst case” scenario (not including prescription coverage).

Pharmacy Out-of Pocket Maximum: This is just like the medical out-of-pocket maximum described above, but only for prescriptions. The 80/20 plan and 70/30 plan both have separate deductibles for prescriptions, while the CDHP plan assigns both medical and pharmacy claims towards the same deductible. This makes it seem like the CDHP plan has better prescription coverage than the 80/20 or 70/30 plan, but those two only apply their deductibles to high tiered prescriptions that aren’t used by very many people. With the 80/20 and 70/30 plans, most of your prescriptions will be a set price for a 30- or 90-day supply, so most people will never really get close to meeting their limits with simple $5 and $30 co-payments per month.

Out-of-Pocket Maximum (Combined Medical and Pharmacy): The basic concept was covered in the previous two sections, but this number represents the “worst case scenario” for all of your out-of-pocket health expenses combined. There is no scenario where an individual will have to pay more than $3,500 on the CDHP plan, $6,850 on the 80/20 plan, or $8,828 on the 70/30 plan. This is a helpful number to know if you’re going to need a major surgery or hospitalization. These numbers are relatively low compared to today’s health insurance environment, where standard maximums are usually around $10,000 or $15,000 annually, so this is a one of the best aspects of the State Health Plan and a major selling point for most people.

ACA Preventive Services: These are the rates for certain services that have been categorized as “preventive” by stipulations in the Affordable Care Act, which has been adopted by the State Health Plan. You can check out the details of what is considered a preventive service on the State’s website – this includes things like your annual wellness exam, most vaccinations, and standard age-based guidelines and screenings. Preventive medicine has been proven to keep people healthier, so insurer’s are making a big push to ensure all of their members get these basic, cost-effective primary care services now so they can avoid having to pay for complicated, expensive hospital visits later. Because the services are preventive, and not urgent, the insurance penalizes you significantly for receiving these services out-of-network, so make sure the provider you see accepts your insurance if you want to receive these benefits.

Office Visits: So far, everything has basically seemed most favorable to the CDHP 85/15 plan. The next few topics are where the real benefits of the 80/20 and 70/30 plans come in, since they have co-payments for most medical services, instead of a deductible. While their deductible may be higher, it also applies to fewer things that you are likely to need. This is also the part of your benefits that applies to appointments at Family Care, if you were wondering.

For example, consider a single primary care visit for the flu – to make it easy, we’ll say its your first visit of the year.

With the CDHP plan, you are paying 100% of the cost of the visit because you haven’t met your deductible yet. This includes the doctor’s visit, flu testing, lab work, prescriptions, and any other services you may need. However, if the visit falls within the first $600 of your annual health expenses, the charges would be paid by your HRA account and you would not owe anything out-of-pocket. You would also get $25 added to your HRA, so you can think of that like a cash-back rebate towards your health expenses for using an in-network provider. After your HRA has been exhausted for the year, you will owe 100% of every office visit you have for the next $900, and 15% after that until you reach your maximum.

With the 80/20 plan, you would only pay a $25 co-payment for a doctor’s office visit, rather than having the charges applied to your deductible and owing 100%. Basically, you would save about $75 every time you went to a PCP and $215 every time you went to a specialist. If you had any testing or additional services (eg. flu test, breathing treatment, etc.), your deductible would apply in addition to your co-payment. This makes things relatively simple and helps people budget costs once they expect to have several office visits each year.

The 70/30 plan has the highest co-payments, but they are still not too far off from the 80/20 plan and the deductible applies to PCP visits the same way. You will have a higher co-payment, but still pay the same rates for additional services towards your deductible.

Urgent Care: Just like the section on Office Visits, but in an Urgent Care setting. There isn’t too much different about the basic process from office visits, so the main thing to notice is how much higher your expenses will be at an urgent care vs. your primary care provider. Whenever possible, you should always try to visit your primary care provider before attempting to go to an urgent care. For example, at this great independent primary care facility known as Family Care, we can guarantee either same-day or next-day appointments, so we can help you avoid the higher costs and lower quality of service that you’re bound to experience at an urgent care facility.

The nice thing is that the benefits for urgent care visits are identical at both in-network and out-of-network providers. Because the problem you are experiencing is obviously “urgent” if you are visiting an urgent care, your insurance company won’t care about the network and allow you to get treated wherever is most convenient. They charge a steep fee for this convenience, but it is still nice to know you won’t be charged more because of the network.

Emergency Room: Again, the CDHP plan applies charges to a deductible, while the 80/20 and 70/30 plan have co-payments associated with the visits. Depending on the significance of your reason for visiting the ER and how close you are to meeting your deductible, either one might be considered the best option for your situation. The one, and probably only, benefit to an ER visit is that you’ll likely go well beyond your entire out-of-pocket in just a few hours, so your healthcare will basically be “free” for the rest of the year. Yay for you!

Inpatient Hospital: This is reserved for actual hospital stays where the patient is admitted and kept in the hospital for some period of time. With all of the plans, you’ll only end up receiving the benefits in this row if you visit the ER and are then later admitted to the hospital. The insurance does not try to charge you twice after an admission, so the bump from an ER visit to an admission is not too drastic. The CDHP and 80/20 plans have an option to either get money back or have their co-payments waived if you visit a Blue Options Designated Hospital, so you should try to visit a preferred hospital whenever possible.

Prescription Coverage: The concept of tiers is pretty complicated, so I will go over this part in a separate post. However, the basics are still pretty much as the regular medical benefits the same across the three options. The CDHP has prescriptions applied to the same deductible as everything else, while the 80/20 and 70/30 plans have co-payments associated with different tiers of drugs. If you aren’t sure what these terms really mean, here is a good 2.5 minute video on what a drug formulary is and why your insurance has grouped different drugs into tiers.

For the State Health Plan, specifically, here are the links to the specific formulary for each plan. You should look up the medications you take to determine what tier they are classified under so you can get a good idea of your expected costs for that drug. The formulary changes all the time and the difference between a Tier 1 drug and a Tier 2 drug could be hundreds of dollars per year, so this helps keep you from being surprised when you show up at the pharmacy.

In my opinion, the State Health Plan is the best health insurance to have in North Carolina. Each plan has their specific benefits and drawbacks, but they are all significantly better insurance plans than the plans you’re likely to find available on Healthcare.gov. The problem is finding the plan that makes the most sense for how it will actually be used by you and your family. Every medical situation is unique, but here are some of the pros and cons of each plan to might help you make your final decision.

CDHP (85/15)

Pros: Potential for $0 premium and includes the lowest cost to add children and/or spouse. If you spend under $600 per person, your out-of-pocket expenses will be paid entirely by your HRA. This plan has the lowest out-of-pocket maximum, so this plan has the best “worst case scenario.”

Cons: You are required to pay for 100% of your expenses between $600 and $1,500 each year. You’ll have to pay for prescriptions under the same deductible as medical expenses. You’ll need to take additional steps to set up your HRA with your employer.

Enhanced 80/20

Pros: Lowest co-payments for PCP and Urgent Care visits, as well as most prescriptions. Pharmacy deductible is only $2,500, so meeting that deductible could help reduce overall costs if prescriptions make up a large percentage of your medical expenses.

Cons: Requires at least $15 per month, minimum, in premiums and has the highest premium cost to add family members. Potentially has the highest cost in a situation where multiple family members need extensive care and prescription coverage.

Traditional 70/30

Pros: Has a lower premium than the 80/20, but still maintains a similar structure for PCP and urgent care visits. Has co-payments for Tier 3 medications, so certain medications might be cheaper than the other plans. One prescription deductible applies to the entire family.

Cons: Has the worst coverage after the deductible has been met of the three plans. Because the premium is similar to the CDHP, while the coverage is similar to the 80/20 plan, the segment of people that would have the best coverage for their unique situations is fairly narrow. Most people would be better off getting the CDHP or 80/20, but there is a definite middle group where this plan makes the most sense.

I hope this was a helpful breakdown of the major components of these three plans. For more details on how you should think about this information, in general, be sure to check out our recent post on the 3 things you should consider when signing up for health insurance.

If you have any questions, please submit them in the comments and I’ll be sure to reply. Thanks for reading!

3 Things to Consider When Signing Up For Health Insurance

The problem that most people have with their health insurance plan is rarely with the actual coverage – people are generally only upset when their plan doesn’t cover something they thought it would or when they are surprised by some costly detail that wasn’t made clear at enrollment. Insurance companies don’t do the best job of educating patients on the actual details of the plans they are selling, but the information you need to know to set proper expectations is available if you know where to look. You’ll have to do some work and learn some pretty boring things, but you are the one who ultimately has to understand the details of your plan’s coverage, not your insurer. The point of this article is to help you understand the crucial differences between possible plans and help you feel comfortable with the coverage you choose.

The entire concept of health insurance is that you are basically making a bet on your health. The healthier you are, the less likely you are to use your insurance for high cost medical services. Your insurance company knows this and sets their prices accordingly. If the insurance company thinks you are going to cost $5,000 to cover this year, their goal is to set your total premiums and out-of-pocket expenses to more than $5,000 so they can make a profit.

This is the bet –who will get the better deal once all of your medical expenses have been paid?

The benefit structure of every plan offered by insurers is carefully calculated to give them the best chance of winning this bet. By understanding how your insurance plan works, you can put the odds back in your favor and make every dollar you have to spend on healthcare go much further.

There are three broad categories to consider when signing up for a new health insurance plan:

Cost – How much will I pay in out-of-pocket expenses?

Coverage – What services and medications will I have access to under my plan?

Network – Is my provider “in-network” with my insurance plan?

Each component is equally important and can have critical implications on the others. While it is almost impossible to get your expected costs 100% right before things actually happen, just having a very good estimate will help you budget accordingly and avoid surprises when you seek medical care. If you need help with this calculation, our Health Insurance Cost Estimator Tool should help give you a good estimate.

I hope the following pages will help you fully understand the benefits, and consequences, of your choices when you’re deciding between two possible plans.

Continue reading to go into further detail on each one of these components.

COST – How much will I pay in out-of-pocket expenses?

The most popular way to think about the cost of your health insurance plan is to focus on the monthly premium. This sounds good because you know the fixed costs associated with your plan and can seemingly predict exactly how much you will have to spend for coverage. However, this line of thinking leaves out the most important part by ignoring the variable costs a person might incur each year when they actually use their health insurance and visit their doctor.

To get a complete picture, you should compare a plan’s total expected out-of-pocket expenses, which factor in the possible copayments, coinsurances, and deductibles that you might have to pay for during the year in addition to your premiums. Signing up for insurance and paying your premiums to your insurer is not the only out-of-pocket expense you should expect if you need medical care. Much like car loan payments don’t cover the cost of the gas you need to put in the car, different health insurance plans might require significantly more “gas” than others if you actually want to take your plan out for a drive.